Shortening the length

Crude oil prices slipped, with ICE Brent front-month prices at reaching 71$/b, as money managers continued to aggressively reduce their net length across WTI & Brent…

European gas prices weakened yesterday, not very sensitive to the drop in Russian flows (down to 229 mm cm/day on average, compared to 252 mm cm/day on Tuesday, probably because of lower offtakes by long term buyers) and in Norwegian flows (down to 319 mm cm/day on average, compared to 333 mm cm/day on Tuesday). Indeed, weak demand, prospects of higher Norwegian production this summer following a permitting decision by the petroleum and energy ministry, enabling an additional 1.4 Bcm of exports, and hopes for a plan to end the Russia-Ukraine war exerted downward pressure.

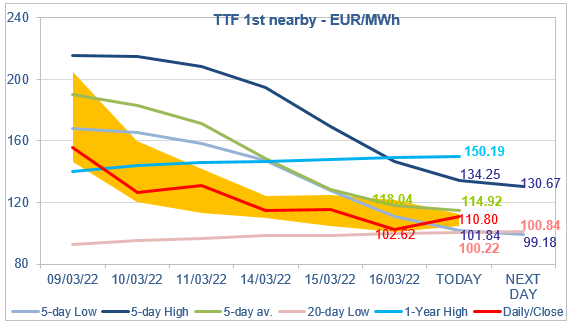

At the close, NBP ICE April 2022 prices dropped by 33.590 p/th day-on-day (-12.24%), to 240.810 p/th. TTF ICE April 2022 prices were down by €12.82 (-11.10%), closing at €102.623/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €5.03 (-7.67%), closing at €60.533/MWh.

In Asia, JKM spot prices increased by 4.53%, to €110.787/MWh; April 2022 prices dropped by 0.73%, to €115.816/MWh.

Finally, the 5-day Low did not manage to lend support to TTF ICE April 2022 prices yesterday which dropped towards the 20-day Low. Prices are rebounding this morning, as both the 5-day Low and the 20-day Low should now lend strong support. The higher levels of Asia JKM prices justify this rebound: despite the expected maintaining of Norwegian production at high levels this summer, Europe will still need high LNG supply, and thus a price premium against Asia. As mentioned in the past days, a price drop towards the coal switching range (whose maximum has fallen to €80/MWh) is difficult to justify for the moment, but it could be a possibility if fundamentals (or the perception market participants have of them) continue to improve.