Physical markets increasingly reflecting summer strength

ICE Brent prices approached 75 $/b yesterday after the EIA weekly data release showed further scarcity in the US crude market. Later in the day,…

Yesterday was a day of transition or “breathing space” on the markets. There was little movement on rates, which even fell slightly in the US (1.86% for the 10-year), while the German 10-year stabilised at around 0%. The US equity market still fell again, with the Nasdaq giving up 1.15%, or more than 10% from its November high. But futures are up. The EUR/USD exchange rate is rising slightly, above 1.1350.

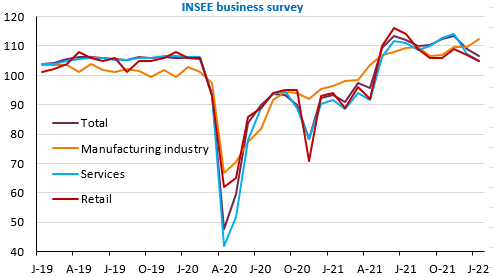

The economic calendar is light: US jobless claims should confirm their rebound and the Philadelphia Fed index may plunge further due to the Omicron wave and its negative effects on activity, but this should not last. The latest INSEE survey in France also confirms the scenario of a moderate slowdown in activity, mainly in services and retail trade.

Producer prices continued to accelerate in Germany at +24.2% yoy, but the ECB continues to expect a sharp decline in inflation this year as confirmed by its President this morning. The account of the last ECB meeting will be published today: we will be able to see if this view is widely shared or intensely debated. The Bank of China lowered its 1 year lending rate from 3.8% to 3.7% and the 5 year rate from 4.65% to 4.6%. This was expected.

Generally speaking, there are few market movers in the economic agenda before the Fed meeting next week, except for the PMIs on Monday.