Equity markets down 20-30% in H1

For the first time since the beginning of the year, US consumer spending contracted in real terms (deflated for inflation) in May, amplifying recession fears and the downward…

European gas prices weakened yesterday, maybe “reassured” by the fact that Europe has decided (at least for the time being) not to follow the United States in banning the import of Russian energy. Yesterday, Russian gas supply continued to flow, averaging 267 mm cm/day (of which 169 mm cm/day on Nord Stream 1), compared to 263 mm cm/day on Monday.

Note that the European Commission published yesterday plans to cut EU dependency on Russian gas by two-thirds this year and end its reliance on Russian supplies of the fuel “well before 2030”. The new plans come on top of climate change policies the EU is currently negotiating, which are designed to cut emissions faster this decade and would alone cut EU gas use 30% by 2030.

In the very short term, The EU will also propose rules by April requiring its member countries to fill gas storage to 90% by 1 October each year (EU storages are currently 27% full).

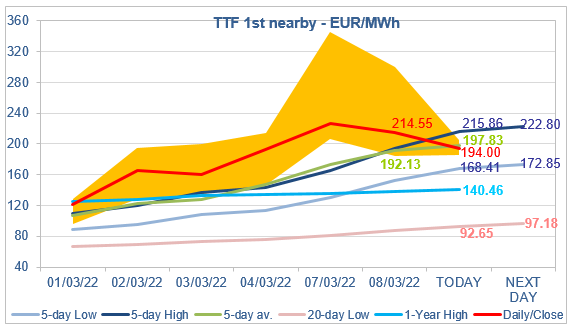

At the close, NBP ICE April 2022 prices dropped by 28.090 p/th day-on-day (-5.21%), to 511.440 p/th. TTF ICE April 2022 prices were down by €12.65 (-5.57%), closing at €214.554/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €2.48 (-2.93%), closing at €82.336/MWh.

In Asia, JKM spot prices dropped by 36.15%, to €173.033/MWh; April 2022 prices dropped by 18.02%, to €133.431/MWh.

TTF ICE April 2022 prices are falling again this morning, back inside their “normal” trading range. Could they drop further, for instance towards the 5-day Low or the 1-Year High targets? An optimistic reading of the EC’s plans might lead one to believe in this scenario. Indeed, to reduce dependency on Russian gas, one of the recommended solutions is to increase LNG imports by around 50 Bcm this year. As a reminder, Europe as a whole (including Turkey) imported 108 Bcm of LNG in 2021, and Asia 373 Bcm. With a world liquefaction capacity that will increase only moderately this year, Europe will need to take the extra 50 Bcm volumes mainly from Asia. This requires TTF prices to stay above JKM prices, ie Asian buyers do not outbid. As we are not sure Asia is able to quickly destroy 50 Bcm of demand, we think that reversing the price uptrend will be difficult to achieve if the risk of an interruption in Russian flows remains.