The price of Brent crude oil has stabilised at around $105/b

There has been very little change in oil prices since their sharp decline following the announcement of the use of US strategic reserves. The price of…

Prices dropped yesterday in most European gas markets, pressured by the additional increase in pipeline supply. Indeed, Russian supply increased again yesterday, to 250 mm cm/day on average, compared to 235 mm cm/day on Wednesday, thanks to the additional rise in flows through Ukraine and the restart of Yamal flows through Poland. Norwegian flows weakened very slightly, averaging 343 mm cm/day, compared to 346 mm cm/day on Wednesday. The drop in Asia JKM prices (-1.80, to €94.534/MWh, for the December 2021 contract) and in parity prices with coal for power generation (thanks to the strong drop in coal prices) also provided bearish pressure.

At the close, NBP ICE December 2021 prices dropped by 7.210 p/th day-on-day (-3.67%), to 189.510 p/th. TTF ICE December 2021 prices were down by €3.17 (-4.14%) at the close, to €73.376/MWh. On the far curve, TTF Cal 2022 prices were down by €1.43 (-2.86%), closing at €48.481/MWh, and the spread against the coal parity price (€32.231/MWh, -2.63%) dropped slightly.

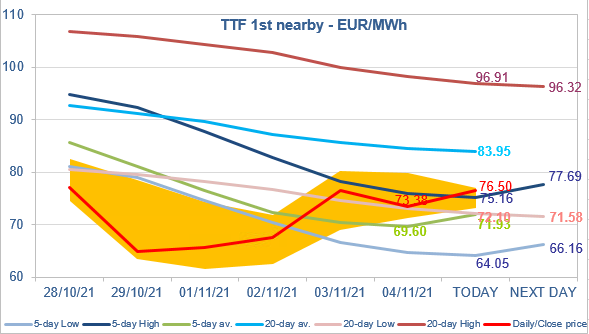

Yesterday, TTF ICE December 2021 prices tried to break above the 5-day High resistance, but the restart of Yamal flows pushed them lower. However, they managed to close slightly above the 20-day Low support. As a reminder, the 20-day Low/20-day High is the “normal” trading range of prices (with the 5-day Low/5-day High range “normally” included inside it). After a period of “abnormality” (i.e. prices in oversold territory), the return to “normal” is causing a slight bullish bias. But, as mentioned yesterday, so that the market does not turn bullish, the 5-day High must continue to set a resistance (scenario of a gradual “normalization”). A break above this resistance level will open the door to the 20-day average, and ultimately to the 20-day High (which is close to Asian prices): for Europe, this would be the worst scenario, meaning European buyers have been obliged again to compete with their Asian counterparts to attract LNG cargoes.