Prices slightly up as Norwegian flows dropped further

European gas prices increased slightly yesterday, supported by the additional drop in Norwegian supply (to 264 mm cm/day, compared to 310 mm cm/day on Monday,…

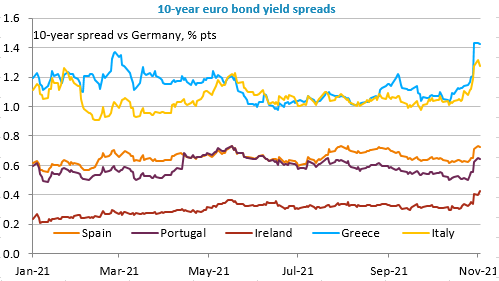

Equity markets started November higher, following an October in which they more than erased September’s losses. Good corporate results in Q3 seemed to show that rising costs were not weighing on margins, but this is only possible if selling prices rise, which supports inflation fears. The ECB meeting last week showed that central banks are finding it increasingly difficult to convince the markets that they will not raise interest rates quickly, and at the same time, bond markets are anticipating that this tightening will weigh on growth, hence the tension on the short end of the yield curve, while longer-term rates are easing. In the Eurozone, concerns are more evident in the widening spreads between German rates and those of southern European countries, particularly Italy and Greece, two highly indebted countries that have benefited greatly from ECB bond purchases.

The positive trend in the equity markets seems to be reversing in Asia and Europe following the publication of China’s PMIs, which were down in October, and the persistence of Covid cases in the country. The ISM industrial survey in the US also confirmed inflationary pressures as key Fed and Bank of England meetings approach this week. And finally, the Biden plan still appears to be stalled by dissent in the US Democratic Party.

Today’s main focus will be on Eurozone manufacturing PMIs, whose first estimate was relatively stable in October. The EUR/USD exchange rate, which had fallen sharply on Friday despite the good growth figures for the Eurozone in Q3, is back around 1.16.