European prices up overall

European gas prices were up overall yesterday, supported by the ongoing concerns on weak stock levels as gas storages remain in net withdrawal mode in…

European gas prices weakened yesterday, pressured by improving spot fundamentals, as shown by storages that have switched to net injection mode for the European Union as a whole. However, some concerns remained on supply for the coming weeks (on Russian and LNG flows), reflected in lower price declines on the far curve. Note that at the monthly auctions held yesterday Gazprom did not book transportation capacity on the Yamal pipeline through Poland, leaving Europe without the assurance of a resumption of Russian exports on this route. Yesterday, Russian flows increased to 220 mm cm/day on average, compared to 214 mm cm/day on Friday.

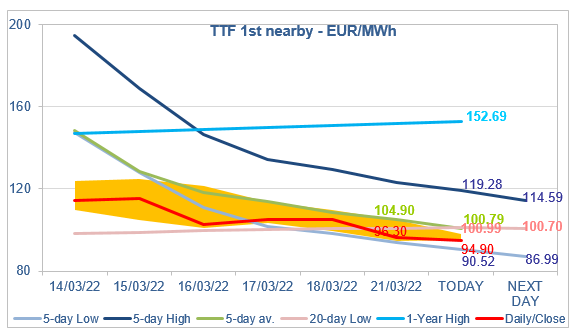

At the close, NBP ICE April 2022 prices dropped by 20.690 p/th day-on-day (-8.41%), to 225.310 p/th. TTF ICE April 2022 prices were down by €8.74 (-8.32%), closing at €96.302/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 76 euro cents (-1.19%), closing at €63.208/MWh.

In Asia, JKM spot prices dropped by 7.08%, to €102.298/MWh; May 2022 prices dropped by 1.56%, to €107.842/MWh.

TTF ICE April 2022 prices dropped yesterday below the 20-day Low support, confirming the market has turned bearish with the 5-day range being now the most relevant trading range. Therefore, a drop towards the 5-day Low (€90.52/MWh for today) is likely. At this level, prices will still be above the coal switching range (whose maximum is currently around €79/MWh). But keep in mind that this 5-day range is wide, the 5-day High being at €119.28/MWh for today. Given the level of Asia JKM prices and the level of the most expensive gasoil substitution possibilities (in the €129-146/MWh range), any tension on fundamentals could push prices strongly up (after breaking the resistance of the 5-day average).