SPECIAL WEBINAR: The storm is raging accros European energy market

EXCLUSIVE WEBINAR Star your free trial & Get access to an exclusive webinar The storm is raging across European energy markets – European gas systems…

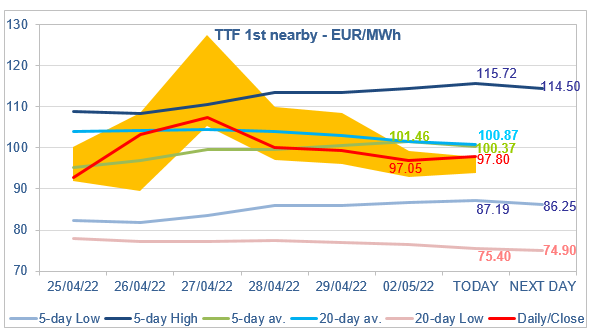

European gas prices were down overall yesterday, pressured by the rise in pipeline supply. Indeed, Russian flows were significantly up yesterday, averaging 260 mm cm/day, compared to 223 mm cm/day on Friday. Norwegian flows were also up, to 317 mm cm/day on average, compared to 304 mm cm/day on Friday.

Note that the European Commission is expected to propose a sixth package of EU sanctions against Russia this week, including a potential embargo on buying Russian oil, with possible exemptions for the most dependent countries.

Moreover, the Commission said that complying with Russia’s proposed scheme (for payment in rubles) in full would breach existing EU sanctions, but promised more detailed guidance on what companies can and cannot legally do.

At the close, TTF ICE June 2022 prices were down by €2.40 (-2.41%), closing at €97.051/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €4.26 (-5.43%), closing at €74.223/MWh.

In Asia, JKM June 2022 prices dropped by 3.86%, to €76.338/MWh.

TTF ICE June 2022 prices maintained their slight bearish bias yesterday in a market marked by low intraday volatility. The level of Asia JKM prices and the level of the maximum coal switching level (86.78/MWh yesterday, very close to the 5-day Low target) suggest prices have additional downside potential. But, concerns on Russian deliveries are limiting the drop for the moment. The EU guidance on the payment in rubles could be the trigger that unlocks all the downside potential… or not.