New spike in risk aversion fuelled by higher bond yields

Risk aversion returned on financial markets yesterday, as a key measure of inflation expectations topped 2.5% in the US, which drove bond yields higher. Yet,…

After a strong start, European gas prices weakened by the close yesterday as the 30 mm cm/day of day-ahead transport capacity at Mallnow booked by Gazprom suggests Russian supply is likely to at least remain flat. The spread with Asia JKM prices (+2.43% on the spot, to €112.127/MWh; -1.24% for the January 2022 contract, to €108.195/MWh) widened slightly. On the spot pipeline supply side, Norwegian flows were slightly down yesterday, at 346 mm cm/day on average, compared to 349 mm cm/day on Monday. The same for Russian supply, which averaged 286 mm cm/day, compared to 285 mm cm/day on Monday.

At the close, NBP ICE January 2022 prices dropped by 1.450 p/th day-on-day (-0.61%), to 236.860 p/th. TTF ICE January 2022 prices were down by 93 euro cents (-1.00%) at the close, to €92.513/MWh. On the far curve, TTF Cal 2022 prices were down by 48 euro cents (-0.86%), closing at €55.256/MWh, with the spread against the coal parity price (€34.860/MWh, -3.88%) widening.

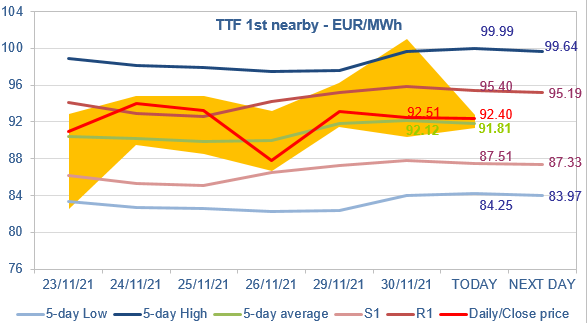

TTF ICE January 2022 prices challenged the 5-day High resistance yesterday before closing around the 5-day average. The volatility of the two last sessions comes mainly from the expiration of the December 2021 contract (with last minute buying). Prices could now stabilize within the S1-R1 range, with an upward bias due to the strong levels of Asia JKM prices.