Another day of muted activity in the power and carbon markets

The NWE power spot prices slightly rebounded yesterday, buoyed by forecasts of lower renewable generation, while an improving nuclear availability kept the French prices steady…

European gas prices increased strongly yesterday, ignoring the continuation of Russia pipeline gas exports to Western Europe (which even increased to 258 mm cm/day yesterday, compared to 247 mm cm/day on Monday). The market seems to realize that Russia is not just a major pipeline exporter but also the world’s fourth largest LNG exporter (behind Australia, Qatar and the US) with 41 Bcm exported in 2021, 8% of world total exports. With companies active in the LNG sector like Shell, BP and now Exxon Mobil deciding to exit the country and withdraw from their partnerships with Russian companies, the sustainability of Russia LNG exports is questioned.

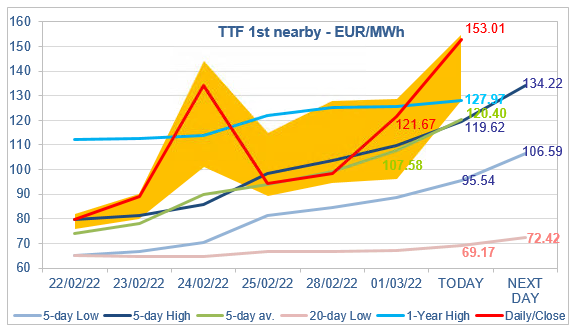

At the close, NBP ICE April 2022 prices increased by 52.200 p/th day-on-day (+21.95%), to 289.980 p/th. TTF ICE April 2022 prices were up by €23.08 (+23.41%), closing at €121.674/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €7.40 (+12.07%), closing at €68.756/MWh.

In Asia, JKM spot prices dropped by 11.68%, to €99.581/MWh; April 2022 prices increased by 13.64%, to €96.605/MWh.

TTF ICE April 2022 prices increased yesterday much more than we thought, but closed below the 1-Year High target. They are rising much above this morning. Of course, this move is backed by fundamentals, ie the prospect of lower Russia LNG supply and stronger competition between Europe and Asia to attract flexible LNG cargoes (particularly as Japanese buyers are also under strong pressure to end their contractual connections with Russia). With the 5-day average now above the 5-day High (a statistically very rare situation), only profit taking by financial participants seems able to calm the upward pressure today.