Dead calm

The situation has not changed much on financial markets that remain calm. Stocks are trading sideways, bond yields and the USD remain rather stable. The…

European gas prices were mixed yesterday. They dropped on the spot and the two front months, pressured by moderate demand, ongoing strong LNG sendouts and profit taking. By contrast, they increased on the rest of the curve, supported by concerns on Russia-Ukraine tensions and the shape of the Asia JKM price curve: to +2.39% on the spot yesterday, to €84.183/MWh; -0.14% for the March 2022 contract, to €78.419/MWh; +4.31% for the April 2022 contract, to €86.815/MWh. It seems the market is more and more factoring the fact that strong competition between European and Asian buyers to attract LNG cargos could resume this summer when the former will need to fill their stocks and the latter to increase gas-fired power generation. A very likely scenario if Russian flows were to be disrupted! Yesterday, Norwegian flows weakened to 341 mm cm/day on average, compared to 348 mm cm/day on Tuesday. Russian supply was up, averaging 216 mm cm/day, compared to 200 mm cm/day on Tuesday, thanks to higher flows through Ukraine.

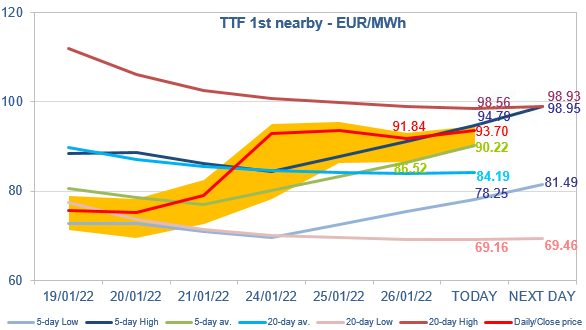

At the close, NBP ICE February 2022 prices dropped by 6.190 p/th day-on-day (-2.75%), to 219.170 p/th. TTF ICE February 2022 prices were down by €1.74 (-1.86%), closing at €91.837/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.82 (+3.63%), closing at €51.865/MWh.

Yesterday, TTF ICE February 2022 prices traded almost perfectly between the 5-day average (which confirms the short-term uptrend) and the 5-day High (a level triggering profit taking from financial participants). Without significant fundamental (or political) news, they could continue to trade in this range today. Indeed, these price levels allow Europe to be the market of choice for LNG while avoiding overbidding (as long as Asian buyers do not increase their bids more aggressively).