Prices have increased their rebound

European gas prices have increased their rebound yesterday, as the statements made by Russia’s Deputy Prime Minister Alexander Novak (saying that commercial gas deliveries via…

European gas prices were mixed yesterday. They dropped on the spot and the near curve, pressured by forecasts of higher temperatures and comfortable pipeline supply. Indeed, Russian flows were slightly down yesterday, averaging 258 mm cm/day, compared to 262 mm cm/day on Friday. Norwegian flows increased to 331 mm cm/day on average, compared to 328 mm cm/day on Friday. By contrast, prices were up on the far curve as the acceleration of Europeans’ efforts to cut dependence on Russian gas will lead them to look for more expensive alternatives, at least initially.

Note that yesterday Germany decided to place under temporary state control Gazprom Germania (an energy trading, storage and transmission business owned until recently by Gazprom) in order to ensure energy security. All voting rights in the company will be moved to the German regulator.

At the close, NBP ICE May 2022 prices dropped by 13.260 p/th day-on-day (-5.15%), to 244.060 p/th. TTF ICE May 2022 prices were down by €2.63 (-2.34%), closing at €109.523/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.41 (+2.06%), closing at €69.595/MWh.

In Asia, JKM spot prices dropped by 6.89%, to €104.817/MWh; May 2022 prices dropped by 4.30%, to €102.489/MWh.

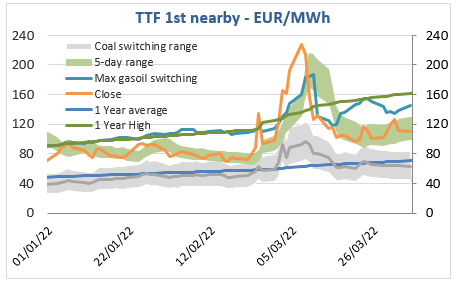

TTF ICE May 2022 prices seem to have found an equilibrium around their current levels. Yesterday, the drop in coal prices and the rise in gasoil prices did not help them to choose a clear direction. They continue to trade almost in the middle of the range set by the maximum coal switching level (currently around €83/MWh) and the maximum gasoil switching level (currently around €145/MWh). Once again, a balanced position between improving spot fundamentals and risks on future supply!