Lower prices in Europe and in Asia

With unchanged fundamentals, European gas prices weakened yesterday, pressured by technical selling. The additional drop in Asia JKM prices and the drop in parity prices…

European gas prices were mixed yesterday as the impact of colder weather was partly offset by still-comfortable supply. In particular, Russian flows were up yesterday, averaging 250 mm cm/day, compared to 245 mm cm/day on Friday. Norwegian flows were stable, at 323 mm cm/day on average.

Note that the Kremlin said yesterday Russia was working out methods for accepting payments of its gas exports in rubles and added it would take decisions in due course should European countries refuse to pay in the Russian currency. The Russian central bank, the government and Gazprom should present their proposals for ruble gas payments to President Putin by March 31.

Meanwhile, energy ministers from the G7 countries rejected the ruble payment demands, agreeing that it would be a “unilateral and clear breach of existing contracts”.

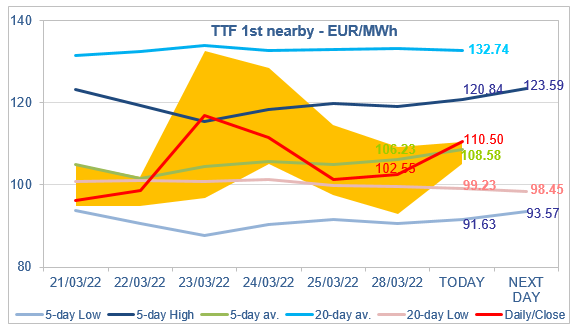

At the close, NBP ICE April 2022 prices increased by 9.160 p/th day-on-day (+3.87%), to 245.770 p/th. TTF ICE April 2022 prices were up by €1.28 (+1.26%), closing at €102.545/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 90 euro cents (-1.31%), closing at €67.371/MWh.

In Asia, JKM spot prices dropped by 6.71%, to €96.390/MWh; May 2022 prices dropped by 1.31%, to €105.585/MWh.

TTF ICE April 2022 prices failed to drop towards the 5-day Low yesterday. As shown by the relative stability of the 5-day average, the market seems to have found an equilibrium around the middle of the range set by the maximum coal switching level (currently around €85/MWh) and the maximum gasoil switching level (currently around €144/MWh). Prices are increasing more noticeably this morning, but the 5-day High could be difficult to reach, particularly as the level of Asia JKM prices does not justify an overbid.