European curve prices continued to increase

European spot gas prices were mixed yesterday, torn between the bullish impact of strong heating demand due to below-normal temperatures and the bearish impact of…

European gas prices were mixed on Friday: rather down on the markets benefiting from strong LNG supply like the UK NBP, rather up on the others. On the pipeline supply side, Russian flows remained stable on Friday, at 104 mm cm/day on average. Norwegian flows increased to 324 mm cm/day on average, compared to 320 mm cm/day on Thursday.

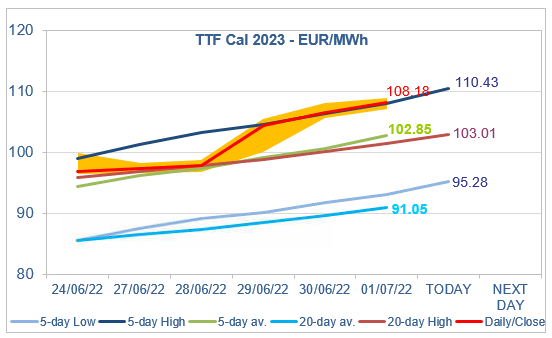

At the close, NBP ICE August 2022 prices dropped by 7.360 p/th (-2.96%), to 240.94 p/th, equivalent to €98.436/MWh. TTF ICE August 2022 prices were up by €3.270 (+2.26%), closing at €147.784/MWh. On the far curve, TTF ICE Cal 2023 prices increased by €1.581 (+1.48%), closing at €108.177/MWh.

In Asia, JKM spot prices increased by 2.25%, to €132.611/MWh; August 2022 prices increased by 0.04%, to €126.549/MWh.

Once again, on Friday, TTF Cal 2023 prices closed at a level very close to the 5-day High. They increased their premium against coal prices (-0.31% for API2 1st nearby prices on Friday, -0.08% for Cal 2023 prices), which continues to fuel the loss of market share of gas compared to coal in the global energy mix (see the Gas & Coal Weekly Report published on Friday). In the absence of a decisive fundamental element, the 5-day High level (€110.43/MWh for today) should continue to set a resistance. So far, profit taking by financial participants failed to pull prices below this level (for instance towards the R1 level, at 107.94/MWh for today), but it is still a possibility.