Far curve prices strongly up after the EU proposed a ban on Russian coal

Gas

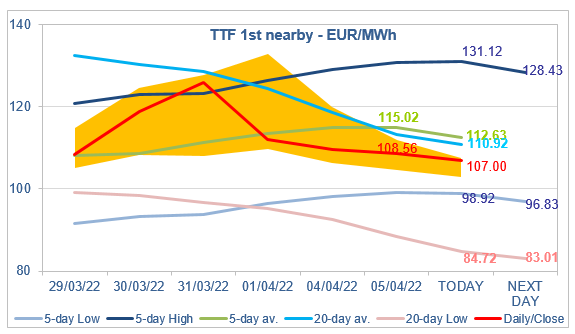

European gas prices were once again mixed yesterday. They dropped slightly on the spot and the near curve, pressured by warmer weather and comfortable pipeline supply. Indeed, Russian flows were stable yesterday, averaging 258 mm cm/day. Norwegian flows dropped slightly to 329 mm cm/day on average, compared to 331 mm cm/day on Monday. By contrast, prices were up on the far curve, supported by the strong rise in coal prices (API2 May 2022 prices increased by 15.84%, and Cal 2023 prices by 13.68%) after the European Union proposed new sanctions against Russia, including a ban on coal imports.

In a longer term perspective, note that the UK government ordered yesterday an expert report on shale gas fracking, saying all energy supply options should be on the table in light of soaring oil and gas prices exacerbated by the Russia’s invasion of Ukraine. It said the current fracking pause in England (a moratorium was imposed in November 2019) would remain in place unless the latest scientific evidence demonstrated that shale gas extraction was safe, sustainable and of minimal disturbance to those living and working nearby. The business minister requested that the British Geological Survey submit the report to him before the end of June.

At the close, NBP ICE May 2022 prices dropped by 1.820 p/th day-on-day (-0.75%), to 242.240 p/th. TTF ICE May 2022 prices were down by 96 euro cents (-0.88%), closing at €108.564/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €4.14 (+5.95%), closing at €73.736/MWh.

In Asia, JKM spot prices dropped by 3.72%, to €100.914/MWh; May 2022 prices increased by 2.16%, to €104.699/MWh.

The strong rise in coal prices pulled the maximum coal switching level significantly higher, to around €92/MWh, compared to €83/MWh on Monday. TTF ICE May 2022 prices initially reacted to the upside, before resuming their downtrend. Indeed, the 20-day average has perfectly played its role of resistance. As we said in our Gas & Coal Weekly Report published yesterday, as long as prices remain below this 20-day average, the bearish trend is confirmed with prices possibly falling towards the maximum coal switching level. Will the latter continue to increase? Not sure because it is the European market which is the most tight, with API2 (ARA) prices trading above API4 (South Africa Richards Bay) and API6 (Australia Newcastle) prices. This means a rerouting of flows can still relieve the European coal market.

The European power spot prices remained stable yesterday amid forecasts of mostly unchanged renewable production and power demand. Prices reached 77.86€/MWh in Germany, France, Belgium…

Concerns about the spread of the Delta variant seem to have significantly diminished suddenly: bond yields rebounded, the US 10y nearing 1.3%. Stock markets were…

Join EnergyScan

Get more analysis and data with our Premium subscription