Short-squeeze drove EUA prices near 90€/t

The European power spot prices inched up yesterday, buoyed by higher clean fuel costs and forecasts of weaker French nuclear availability and German wind production.…

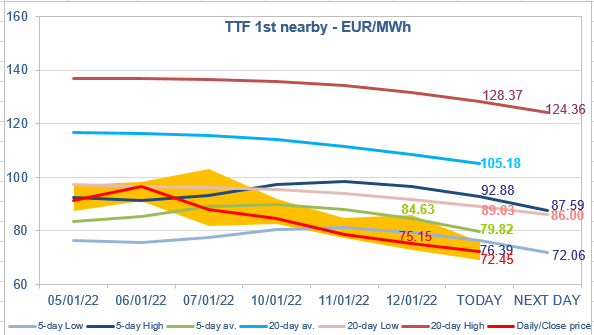

European gas prices maintained their bearish momentum yesterday. Indeed, the movements in Asia JKM prices (+1.42% on the spot, to €81.051/MWh; -0.43% for the February 2022 contract, to €98.410/MWh; -10.30% for the March 2022 contract, to €68.977/MWh) suggest that, while there is still some spot tension in the Asian market, this situation is not expected to last, which should maintain a comfortable LNG supply for Europe. The trend on the pipeline supply was unchanged yesterday. Norwegian flows were slightly up, averaging 342 mm cm/day, compared to 341 mm cm/day on Tuesday. Russian supply was stable at 183 mm cm/day on average.

At the close, NBP ICE February 2022 prices dropped by 10.250 p/th day-on-day (-5.39%), to 179.980 p/th. TTF ICE February 2022 prices were down by €3.58 (-4.55%), closing at €75.153/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €2.17 (-4.77%), closing at €43.295/MWh.

Technical buying was not enough to keep TTF ICE February 2022 prices above the 5-day Low yesterday. They are extending their drop this morning, below this level. The level of Asia JKM prices for March 2022 (which becomes the 1st nearby contract from today) offers additional downside potential. Moreover, Indonesia has allowed today 37 loaded coal vessels (including the 14 ships whose clearance was announced earlier in the week) to depart for exports, which should alleviate Asian buyers’ concerns. However, to play the downtrend while avoiding oversold situations, financial participants could be careful not to sell at a level too much below the 5-day Low of the next trading day.