No clear trend on financial markets, except in Turkey

The slight decline in US bond yields contributed to restore some calm on financial markets, but the trend was not confirmed in Asia overnight. As…

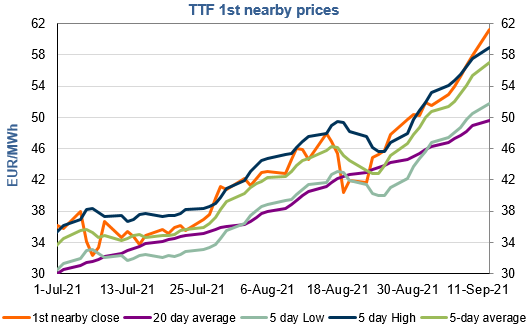

European gas prices continued their (seemingly endlessly) rise yesterday, still supported by concerns on the start date of the Nord Stream 2 gas pipeline. Indeed, the German energy regulator said yesterday that the application by Nord Stream 2 AG for approval as an independent transmission system operator is now complete, and added that it has up to four months from September 8 to produce a draft decision on the application.

The rise in Asia JKM prices (+6.72% on the spot, to €62.525/MWh) and in parity prices with coal for power generation (thanks to higher coal prices) provided additional upward pressure.

On the spot pipeline supply side, Russian flows were almost stable yesterday, averaging 298 mm cm/day (compared to 297 mm cm/day on Friday), still below the levels of end August (313 mm cm/day). Norwegian flows dropped, to 282 mm cm/day on average, compared to 295 mm cm/day on Friday.

At the close, NBP ICE October 2021 prices increased by 7.740 p/th day-on-day (+5.32%), to 153.260 p/th. TTF ICE October 2021 prices were up by 336 euro cents (+5.81%) at the close, to €61.279/MWh. On the far curve, TTF Cal 2022 prices were up by 131 euro cents (+3.48%), closing at €38.903/MWh, increasing the spread against the coal parity price (€35.681/MWh).

Competition between European and Asian buyers to attract the needed LNG cargoes seems to have started, with no known limit. Once again, only (temporary) profit taking by financial participants (who don’t want to suffer a price collapse that would result from an unexpected start of Nord Stream 2) and technical resistances seem able to calm the upward pressure.