Energy prices in the grip of the COVID-19 outbreak

The EnergyScan team held its quarterly webinar covering key trends and events on energy markets. In this webinar, our experts addressed the following topics, with…

European gas prices weakened yesterday, pressured by the rebound in Norwegian flows, which were back to normal, reaching 351 mm cm/day on average, compared to 293 mm cm/day on Wednesday. Russian supply was almost stable, at 279 mm cm/day on average, compared to 280 mm cm/day on average on Wednesday. However, the stabilization in Asia JKM prices at high levels (+0.79% on the spot, to €105.529/MWh; +0.54% for the January 2022 contract, to €106.320/MWh) helped to limit the extent of the decline.

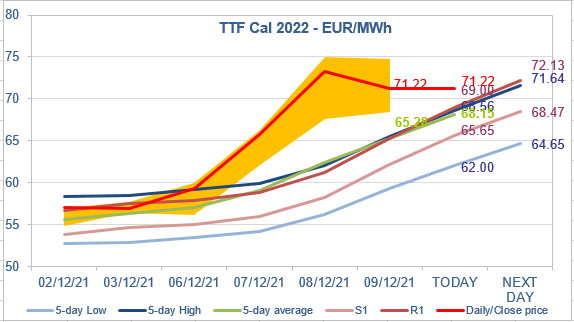

At the close, NBP ICE January 2022 prices dropped by 4.220 p/th day-on-day (-1.62%), to 256.110 p/th. TTF ICE January 2022 prices were down by €1.06 (-1.04%) at the close, to €100.445/MWh. On the far curve, TTF Cal 2022 prices were down by €2.04 (-2.78%), closing at €71.217/MWh, with the spread against the coal parity price (€39.013/MWh, -5.19%) remaining stable.

TTF ICE January 2022 prices closed yesterday between the R1 and 5-day High levels. As for Cal 2022 prices, although they remained above the 5-day High, their drop suggests that some bulls are well aware that prices are overbought and that they consider it more prudent to take their profits at least partially. We still expect them to drop below the 5-day High. However, as the trend is strongly upward, this 5-day High is rising: €68.56/MWh for today, but estimated at €71.64/MWh for the next trading day (Monday) if we assume prices will close today at their yesterday close. This means that for the short-term players who want to buy today to resell on Monday, there is still some money to make, but not so much. For bigger gains, they must keep their position longer and hope that the trend remains bullish. It’s a little more risky.