Markets resolve to consider much less favourable scenarios

Macro & Oil Podcast #23 In this episode of the weekly EnergyScan podcast about the Macro & Oil market, Olivier Gasnier tells us about the…

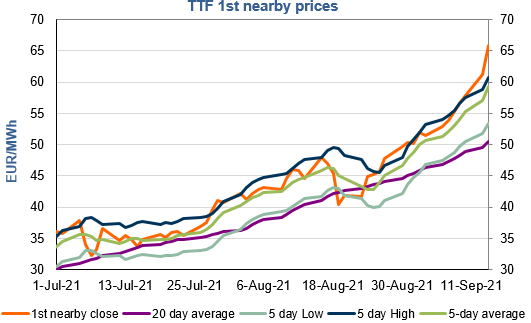

European gas prices continued their (endless?) rise yesterday, still supported by concerns on the commercial start date of the Nord Stream 2 gas pipeline. As a proof that there is now a strong competition between European and Asian buyers to attract the needed LNG cargoes, prices were more sensitive to the rise in Asia JKM prices (+5.42% on the spot, to €65.911/MWh) than to the drop in parity prices with coal for power generation (both coal and EUA prices were down). Additional support came from the closure of the Freeport LNG liquefaction plant in the US due to power issues caused by Hurricane Nicholas.

On the spot pipeline supply side, Russian flows were significantly up yesterday, averaging 312 mm cm/day (compared to 298 mm cm/day on Monday), almost back to the levels of end August (313 mm cm/day). By contrast, Norwegian flows dropped, to 242 mm cm/day on average (compared to 282 mm cm/day on Monday), due to planned maintenance works.

At the close, NBP ICE October 2021 prices increased by 11.690 p/th day-on-day (+7.63%), to 164.950 p/th. TTF ICE October 2021 prices were up by 448 euro cents (+7.32%) at the close, to €65.764/MWh. On the far curve, TTF Cal 2022 prices were up by 153 euro cents (+3.92%), closing at €40.429/MWh, increasing the spread against the coal parity price (€35.221/MWh).

There is no (known) objective limit to gas prices. Profit taking by financial participants and technical resistances have failed so far to calm the upward pressure. The market needs concrete elements on an increase in Russian flows in the coming weeks (via Nord Stream 2 or the existing routes).