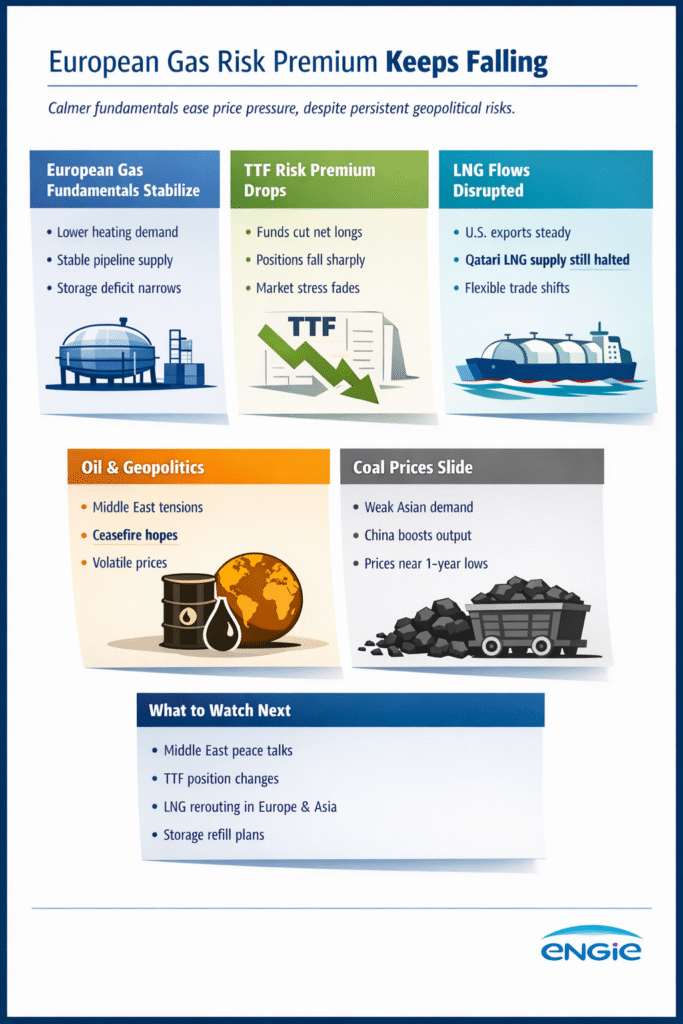

European gas prices eased in April so far as risk premium declined, supported by hopes of a ceasefire agreement in the Middle East, steadier balances, lower storage pressure, and lighter fund positioning.

Since early April, European gas prices had continued to ease as the market risk premium gradually declined. With no further deterioration in the European gas balance during the period under review, speculative positioning adjusted and near-term price support weakened, despite ongoing geopolitical uncertainty.

European Gas Prices: Risk Premium Eased in April.. So far

This analysis reflects market conditions observed up to Friday 17 April, before the rebound seen at the start of the new week due to renewed tensions in the Hormuz Strait after a brief reopening of maritime traffic.

European gas markets extended their recent correction through mid-April, as the perceived risk embedded in prices continued to fall over the period under review. The easing reflected a combination of relatively stable domestic fundamentals, reduced storage pressure, and a gradual unwinding of speculative long positions on the TTF.

While geopolitical risks remained present, they did not translate into any further tightening of the European gas balance during that period.

Stabilising Fundamentals Limited Upside Risk

Through mid-April, the European gas balance did not deteriorate further. Lower heating demand and higher pipeline supply contributed to an improvement in fundamentals, helping to reduce pressure linked to storage refilling.

On 15 April, EU gas storage levels stood at 29.56% full, compared with 35.97% at the same point last year. Although inventories remained below historical levels, the short-term trend helped ease immediate market concerns. At the policy level, the European Commission also reiterated its intention to coordinate storage refilling across member states in order to avoid simultaneous procurement pressures, echoing lessons learned from 2022.

During this period, the relative stabilisation in fundamentals limited the need for additional risk pricing in near-term gas contracts.

LNG Flows Adjusted, but Supply Stayed Constrained

Global LNG flows remained under pressure. U.S. LNG exports continued at strong levels, helping to offset part of the lost Qatari volumes. However, this was not enough to prevent a significant decline in overall LNG supply, forcing buyers to adapt.

China, the largest buyer of Qatari LNG, continued to reduce imports by relying more heavily on domestic production, which rose by 3.17% year-on-year in March to 23.40 Bcm. India, by contrast, had fewer alternatives and turned to more unconventional supply options, including sanctioned LNG volumes.

European buyers responded in the short term by seeking alternative LNG sources, while also considering longer-term diversification strategies. Some market participants explored Canadian LNG supply routes despite higher costs and longer transit times, reflecting a broader reassessment of supply security in the wake of recent geopolitical tensions.

Speculative Positioning Pushed the Risk Premium Lower

The clearest signal of declining risk premium came from investment fund positioning. As the European gas balance stopped worsening during the period, funds continued to reduce their net long exposure to TTF.

During the week ending 10 April, net long positions fell by 37 TWh to 271 TWh, down from a peak of 323 TWh reached on 27 March. This reduction appeared to reflect profit-taking rather than a full reversal in market sentiment.

A more pronounced price decline could have materialised if remaining long positions had been liquidated further. However, such a move would likely have required clearer geopolitical de-escalation. In the absence of that, funds could also have re-entered the market and reintroduced volatility.

Coal and Oil Offered Only Limited Support

Coal markets offered little upward support to gas prices during the same period. Global coal supply remained comfortable, while demand was seasonally weak. API2 and API6 prices maintained a bearish trend and appeared to be moving closer to their one-year averages, offering only limited support.

Oil prices were volatile, driven by shifting expectations around Middle East tensions and possible diplomatic developments. Even so, oil market moves did not materially alter the gas market trajectory through mid-April, as European gas pricing remained primarily driven by gas-specific fundamentals and positioning.

A Market Snapshot, Not a Forward Certainty

As this analysis is based on market developments through Friday 17 April, it should be read as a snapshot of the easing trend observed up to that point. The rebound seen afterward suggests that sentiment remains highly sensitive to new geopolitical or macro signals.

In other words, the earlier decline in risk premium reflected a temporary stabilisation in market conditions rather than a definitive resolution of underlying risks.

Key takeaways

- Up to Friday 17 April, European gas risk premium eased as the market balance stabilised and storage pressure softened.

- Investment funds reduced net long TTF positions, reinforcing short-term downside pressure during the period.

- LNG supply remained constrained, but conditions through mid-April did not justify stronger upside pricing.

- The rebound seen afterward shows that market sentiment remains fragile and highly reactive.

Conclusion

Through mid-April, European gas prices eased not because risks disappeared, but because they stopped intensifying over the period. However, the rebound seen at the start of the following week is a reminder that the market remains highly reactive to new signals and that any easing in the risk premium can quickly reverse.

keywords

European gas prices ,TTF risk premium ,EU gas storage ,LNG supply Europe ,Gas market volatility ,TTF fund positioning ,European energy market