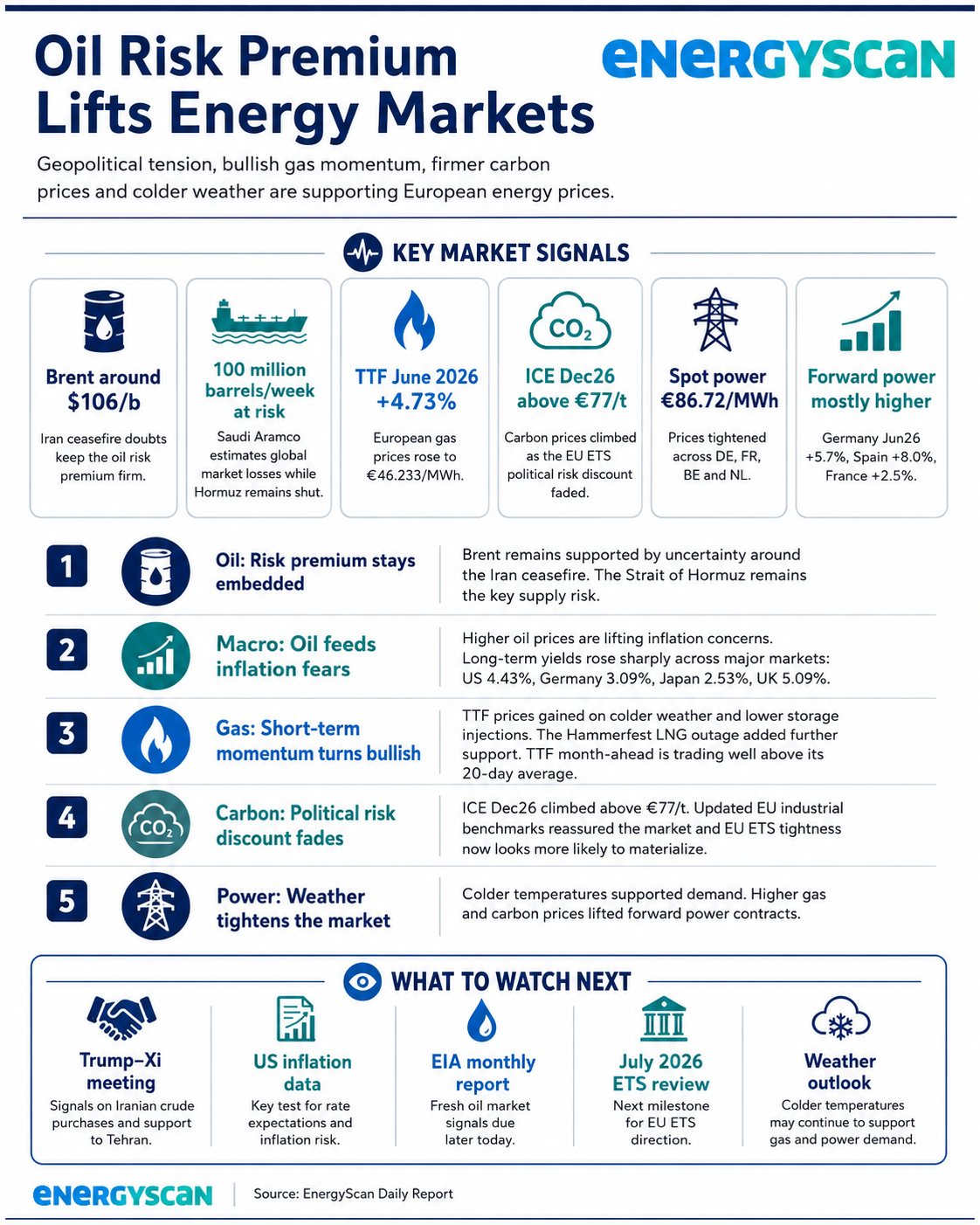

Energy markets remain driven by geopolitical risk, with oil prices rising as uncertainty around the Iran ceasefire continues to support a strong risk premium. The move is spreading across European gas, power and carbon markets, while higher oil prices are also feeding inflation concerns and pushing long-term interest rates sharply higher.

Oil Risk Premium Lifts Gas, Power and Carbon Markets

Oil remains bid as Iran ceasefire doubts intensify

The rebound in oil prices continues as geopolitical risk stays at the centre of market pricing. Brent’s first-nearby contract rose by 2.9% yesterday and opened this morning at $104.23/b, before trading around $106/b.

The key driver is renewed uncertainty over the Iran ceasefire. After the US President described Iran’s response to the US peace plan as “totally unacceptable”, he said the ceasefire was on “massive life support”. This has increased expectations of a potential resumption of hostilities and prolonged the effective closure of the Strait of Hormuz.

The market is therefore maintaining a persistent geopolitical risk premium. Negotiations remain difficult, particularly around Iran’s nuclear programme, sanctions relief, the US naval blockade and the Strait of Hormuz, where Iranian authorities now claim a right of control.

Physical supply constraints remain significant

The report highlights that physical constraints are now clearly quantified. Saudi Aramco stated that global markets are losing around 100 million barrels per week while Hormuz remains shut.

Saudi Arabia has redirected significant volumes via its western Yanbu terminal, but buyers are taking fewer barrels and some flows remain stranded. Saudi crude exports to China for June loading are expected to fall to 13–14 mb, compared with a typical 40–50 mb per month before the Iran war.

Policy responses remain focused on cushioning prices rather than restoring disrupted flows. The US has awarded 53.3 million barrels from the Strategic Petroleum Reserve for release between June and August, following earlier drawdowns that reached a record 1.22 million b/d last week.

The Trump–Xi meeting starting tomorrow is the key short-term diplomatic variable. Any credible Chinese commitment to curb Iranian crude purchases and financial support to Tehran could improve the outlook for de-escalation. A lack of concrete signals would reinforce a prolonged standoff and keep the oil risk premium embedded in prices.

Higher oil prices push long-term yields upward

Rising oil prices are also feeding inflation fears. These concerns have been amplified by the upcoming US April inflation data, with Bloomberg consensus expecting headline inflation to rise from 3.3% to 3.7% year-on-year and core inflation to edge up from 2.6% to 2.7%.

Long-term yields have risen sharply: 4.43% for the US 10-year, 3.09% for the German 10-year, 2.53% for the Japanese 10-year and 5.09% for the UK 10-year. The market is now pricing in a 33% chance of a US rate hike before year-end.

For energy market participants, this reinforces the link between commodity risk, inflation expectations and financing conditions.

European gas momentum turns bullish

European gas prices extended gains yesterday across spot and forward markets. TTF June 2026 rose by 4.73% to €46.233/MWh, while TTF Cal 2027 gained 3.31% to €37.355/MWh.

The short-term momentum is described as rather bullish. Colder weather supported gas demand in Local Distribution Zones, while lower demand from power generation partly offset the move. European net storage injections fell yesterday, and the unplanned outage at Norway’s Hammerfest LNG plant added further support.

Asian gas prices also increased, with JKM June 2026 up 0.44% to €49.07/MWh, now trading at a discount to Europe when shipping is included. In the US, Henry Hub June 2026 rose by 5.55% to $2.910/MMBTU.

A notable LNG signal came from the Qatar-owned Al Kharaitiyat tanker, which crossed outside the Strait of Hormuz after loading in Qatar. The report suggests this may reflect Pakistan’s success in negotiating passage for contractual LNG volumes from Qatar.

Carbon prices rise as political risk discount fades

Carbon prices also strengthened. ICE Dec26 rose by 2.66%, climbing above €77/t, while UK ETS Dec26 jumped by 6.51% to a three-month high.

The EU ETS move followed the European Commission’s updated benchmarks for industrial sectors for 2026–2030. The market was reassured that benchmark reductions were not too dramatic, implying that EU ETS tightness is now more likely to materialise as the political risk discount erodes.

For UK ETS, the move was supported by rising expectations of a possible EU–UK linkage of carbon schemes. Traders are now watching the July 2026 ETS review by the European Commission.

Power prices supported by gas, carbon and colder weather

Spot power prices are averaging €86.72/MWh for delivery today across Germany, France, Belgium and the Netherlands. Weather has tightened significantly compared with 10 days ago, with temperatures below seasonal averages and potentially falling to 5°C below normal in the coming days.

Forward power products were mostly higher, supported by rising gas and carbon prices. Gains were uneven across front-month products: France rose by 2.5%, while Germany gained 5.7% and Spain Jun26 base increased by 8%.

Key takeaways

- Oil markets remain supported by a strong geopolitical risk premium linked to Iran ceasefire uncertainty and the continued disruption around the Strait of Hormuz.

- European gas momentum is bullish, supported by colder weather, lower storage injections, the Hammerfest LNG outage and higher oil-linked risk sentiment.

- Carbon and power markets are also firmer, with EU ETS political risk fading and forward power prices supported by higher gas and carbon prices.

Conclusion

Today’s EnergyScan report points to a broad risk-on move across energy markets, led by oil and transmitted into gas, carbon and power. For energy professionals, the main focus remains the durability of the Iran ceasefire, the evolution of Hormuz-related supply constraints, and the knock-on effects on inflation, rates and European energy pricing.