Russia and Iran erased previous losses

Yesterday was a choppy session for oil, at the end prices went up: ICE Brent front month moved +1.1% higher to $119.81/b and WTI NYMEX…

While the Fed had done everything to limit the reaction of the interest rate markets to its decision to reduce its asset purchases, the Bank of England took them by surprise by leaving its key rate unchanged, even though it had largely contributed to fueling expectations of an increase. A tightening still appears possible in December, but the BoE has mainly sent the message that expectations were too aggressive for 2022. This has caused not only the entire UK yield curve to fall, but also those of other countries. For example, the market now only sees the 2nd Fed rate hike coming at the very end of 2022.

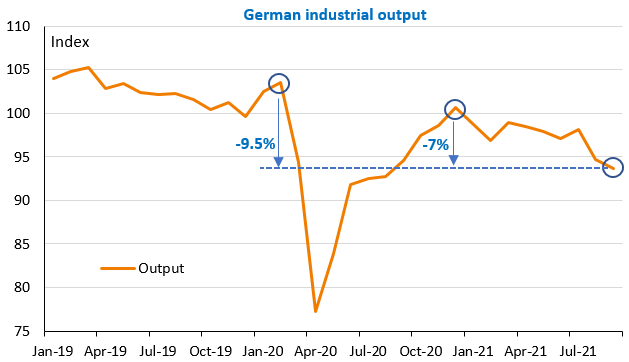

The new drop in German industrial production in September (the 7th since the beginning of the year!) underlines the risks to growth due to supply problems, particularly in the automotive sector. And this should reinforce the caution of central banks. But at the same time, it fuels inflationary pressures because demand is strong.

In this respect, a new reversal in the bond market cannot be ruled out today with the release of the US job report: both the ADP estimate of private employment and the fall in unemployment claims suggest that the consensus (+450k) is too low. In addition, wages are expected to continue to accelerate.

The USD has strengthened quite significantly, both against the British pound of course (GBP/USD @ 1.35) and against the euro (1.1560).