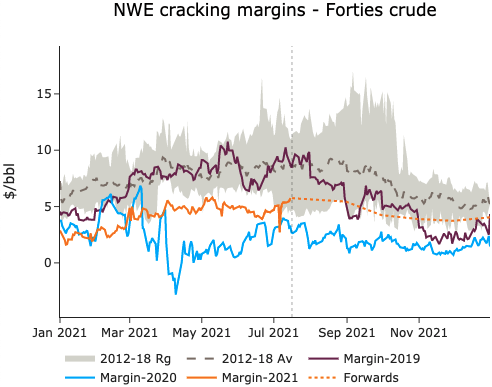

With another decline in crude oil prices, especially at the prompt, and product prices remaining supported, European refiners are back closer to their average profitability levels. Indeed, ICE Brent crude futures declined further, to reach 73.1$/b for September delivery. The time structure also weakened, at 67 cents. Yet, product prices, especially light ends such as naphtha and gasoline, remained supported by European demand and exports. As a result, margins are increasingly within the 5y average range, despite diesel cracks remaining below historical norms.

ARA inventories continue to reflect this uneven scarcity across refined products. Naphtha and gasoline stocks plunged this week by 1.5 mb combined. Following the historic floods in Germany, this decline could persist, as rising Rhine water levels are making it impossible to ship barges of refined products (coming from inland refineries in Germany) through the river. Diesel stocks remained constant last week, while jet fuel stocks remained elevated, despite rising European flight numbers.

The correction of the equity markets continues in the wake of the violent fall of the Nasdaq yesterday evening (-3.34%). Long-term bond yields also continue to rise: the…

European gas prices maintained their bullish momentum yesterday as weak supply and low stock levels continued to raise concerns. Although Russian flows continued to rebound,…

European gas prices continued to increase yesterday, still supported by concerns on supply. Russian flows stabilized at their weak levels yesterday, averaging 104 mm cm/day.…

Join EnergyScan

Get more analysis and data with our Premium subscription

ARA inventories continue to reflect this uneven scarcity across refined products. Naphtha and gasoline stocks plunged this week by 1.5 mb combined. Following the historic floods in Germany, this decline could persist, as rising Rhine water levels are making it impossible to ship barges of refined products (coming from inland refineries in Germany) through the river. Diesel stocks remained constant last week, while jet fuel stocks remained elevated, despite rising European flight numbers.