European prices rebounded

Prices rebounded yesterday in most European gas markets, supported by higher heating demand due to below-normal temperatures and lower pipeline supply. Indeed, due to maintenance…

The strong easing of gas and oil prices has allowed a slight easing of long rates. In addition, the fear of a US default is receding in the short term as both Republicans and Democrats seem ready to raise the debt ceiling until the end of the year. The debates on the Biden plans (infrastructure on the one hand, social and fiscal on the other) will resume. European equity markets fell sharply, but the trend was reversed in the United States and the rebound was confirmed in Asia and now at the opening of the European markets.

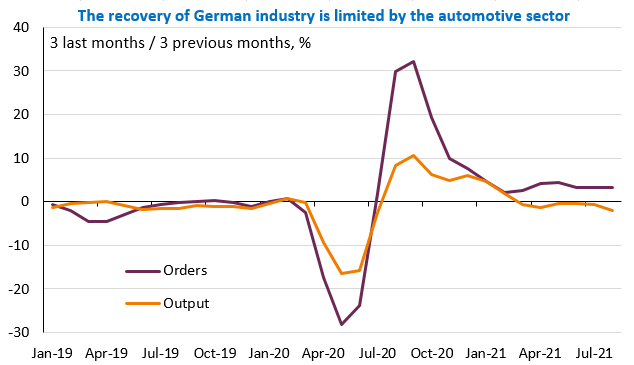

On the economic front, the ADP survey showed 568k private sector jobs created in the US in September, which seems to guarantee good employment figures tomorrow and therefore an announcement of the start of the Fed’s asset purchase reduction as early as November 3rd. On the other hand, Europe was a bad surprise with the sharp decline in German production in August (-4% m/m), which is probably once again linked to the automotive sector, whose activity is restricted by the shortage of semiconductors. German GDP growth estimates for Q3 will be revised sharply downwards.

“>

“>Today: energy prices of course, US jobless claims figures and the budget and debt talks in the US Congress. The recovery of the EUR/USD exchange rate (which touched 1.1529 and is now trading around 1.1570) could be hampered by the poor German figures.