Gas & Power Report: Muted demand and comfortable stocks to weigh on energy prices

Gas & Power Podcast #40 In this week’s podcast, Julien Hoarau discusses about recent trends in wholesale energy markets, with muted demand, global macroeconomic factors,…

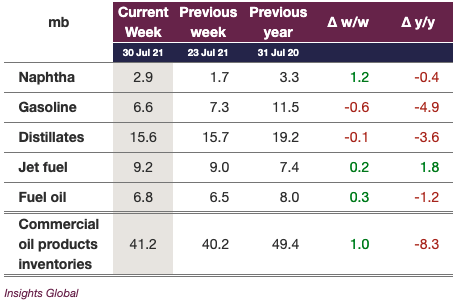

Crude oil prices in Europe and the US continued to climb, to reach 76 $/b for the ICE Brent September contract. On the opposite of the spectrum, INE crude, Shanghai’s medium sour crude future expired for September’s contract at a significantly lower level than previous trading sessions, likely to reflect the growing concerns around a recent outbreak of COVID cases in the Jiangsu province. In Europe, constructive inventory data for transportation fuels (gasoline, jet fuel and diesel) in the ARA region support crude pricing at the prompt, while Singapore inventory data showed a more uneven trajectory. Indeed, European gasoline stocks continued to draw by 0.6 mb, to drop below the 5-year average in the ARA region, while gasoil stocks declined by 0.1 mb. Naphtha stocks jumped by 1.2 mb, despite the tightness of the naphtha market. Significant backwardation in the naphtha market indicates that this upward inventory move is unlikely to persist, amid strong petrochemical margins.