Optimism returns to the markets but rates continue to rise

The temporary deal on the US debt ceiling also gives the Democrats time to agree on the stimulus packages that the Biden administration wants to push through.…

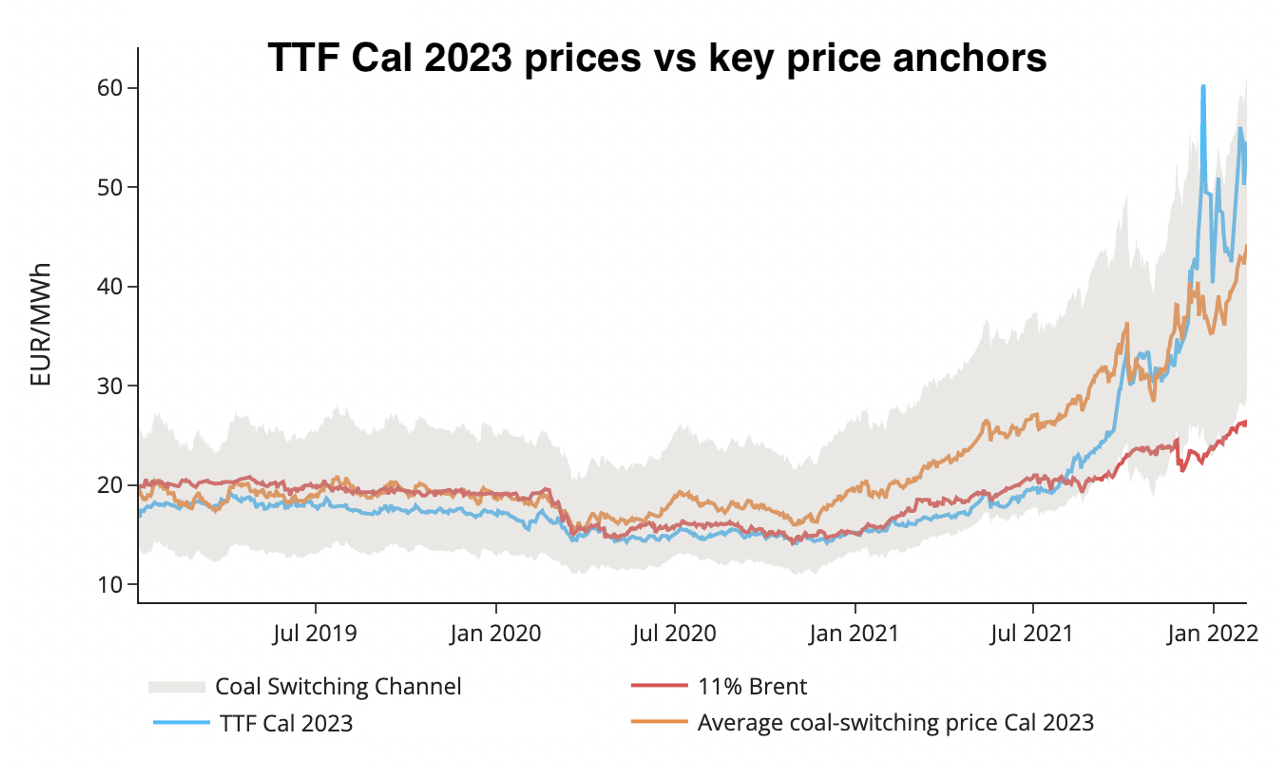

European gas prices ended the week on another bullish note on Friday, supported by a further drop in Russian gas flows through Ukraine and prospects of higher gas demand as temperatures were expected to normalize by mid-February. Strong Brent, oil and coal prices provided support to the far curve as well, with TTF Cal 23 prices remaining close to recent all-time highs towards the €55/MWh mark and still in the upper part of the coal-to-gas switching range.

Expectations of the return of above-average temperatures next week and a jump in nominations for Russian gas imports at the Velke Kapusany entry point to 80 mm cm/day for today dragged European gas prices down at the opening. The results of the quarterly transport capacity auction (at 12:00 CET) could have some impact as well, notably regarding capacity booked at delivery points for Russian gas (Mallnow and Velke Kapusany mainly). The outcome of Biden/Scholz in Washington and Putin/Macron in Moscow meetings over the Russia-Ukraine-NATO crisis will be closely watched by market players today who will look after concrete signs towards a de-escalation process in the Russian military build-up at the Ukrainian border.