Special episode : Understanding the EUA price correction

Understanding the EUA price correction Description February, 24 2026 Special episode Since mid January, EU carbon prices have experienced a sharp correction, falling more than…

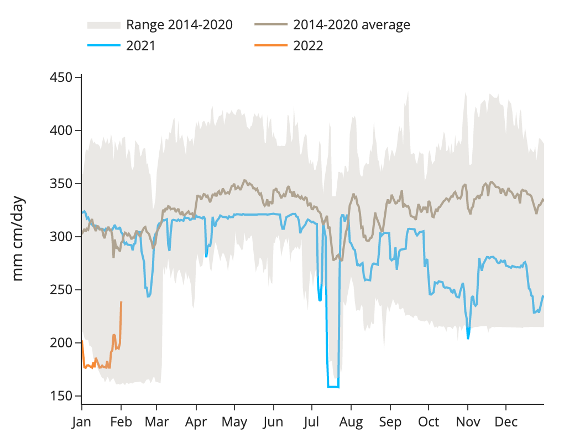

A 40 mm cm/day increase in Russian gas flows to Europe through Ukraine and Nordstream 1 pushed European gas prices further down on Tuesday, eroding again the risk premium built last week. Mild and windy weather continued to weigh on gas demand : UK CCGTs consumed only 33 mm cm of gas yesterday, compared to 59 mm cm/day on average in January while UK wind power generation was above 13 GW on average yesterday compared to 8 GW on average in January. Note that Europe LNG imports hit an all-time high in January at 15.6 Bcm with still dozens of cargoes expected to unload at regas terminals in the coming two weeks. More than 60% of US LNG exports headed to Europe in January 2022, compared to only 21% a year ago.

Nominations for Russian gas imports at the Velke Kapusany entry point are down this morning to 63 mm cm/day, 17 mm cm/day lower day-on-day probably as spot prices dropped significantly yesterday. A downward revision in temperature forecasts for the end of next week could also be supportive and halt the bearish move observed over the past two days. Nevertheless, strong LNG imports and below-average demand in the short term could continue to keep a lid on prompt contracts and limit the rebound potential.