Markets regain some optimism

The equity markets rebounded sharply and long rates rose yesterday, mainly on the confirmation of good news about the Omicron variant, which is proving to be very…

Bulls took control of crude oil prices on Tuesday, supported by reports of falling crude production in Russia (to its lowest level since July 2020 below the 10 Mbd mark on Monday according to Reuters) and a cautious easing of lockdown restrictions in Shanghai. Brent 1st nearby traded as high as $105.60/b intraday.

In its monthly report, the OPEC cut both its 2022 forecast of Russian liquids production by 0.53 Mbd and its 2022 demand growth forecast by 0.48 Mbd, citing soaring inflation rates as the main source of this downward revision. The fact that the OPEC increase its output by only 57,000 bpd to 28.56 Mbd in March, well below the 253,000 bpd rise that OPEC is allowed under the OPEC+ deal may have also played into the bullish sentiment.

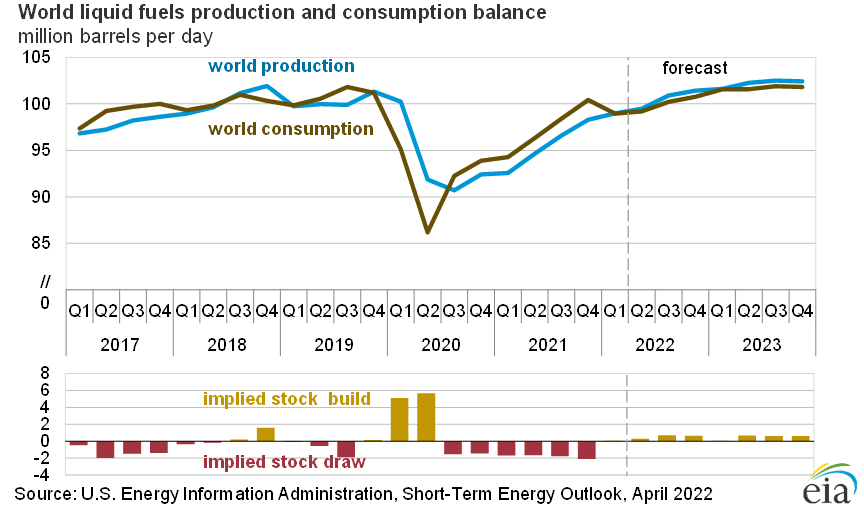

The second monthly report of the day was released by the US EIA and it revealed that the US government expects its crude oil output to rise by 820,000 barrels per day to 12.01 Mbd in 2022 and by a further 940,000 bpd to 12.95 Mbd in 2023, in line with pre-Covid levels. Regarding Russia’s crude oil production, the EIA forecasts that it will decline by 1.7 Mbd from February 2022 to the end of 2023. But overall, the EIA market outlook is rather balanced with increasing production expected to lead to net stock builds until the end of 2023 (see below chart).