Prices up again on higher coal and oil prices

European gas prices were up again yesterday, supported by the additional rise in coal prices (+10.31% for API2 1st nearby prices; +8.72% for Cal 2023 prices).…

Crude markets continued to be partially bid up with ICE Brent November contract reaching 75.4 $/b. The industrial survey published by the API reported another sizable crude draw of 6.1 mb in the US, while gasoline and distillate stocks respectively declined by 0.4 mb and 2.7 mb. The long-lasting impact of Ida on US offshore production, therefore, continues to impact crude markets. A cumulative 29 mb of crude has been lost now due to shut-ins following Ida’s landfall.

However, WTI futures had an extremely weak expiry yesterday, with the front-month time spread compressing close to zero at the close, with only 10 mb physically settled, reflecting the lack of demand at the Cushing hub. US light sweet crude demand appears to be thin, likely due to exports being disrupted due to the hurricane season. Indeed, US refiners mostly process heavy crude but export light sweet crude as their refining kit is optimized to extract value from heavy and sour crudes.

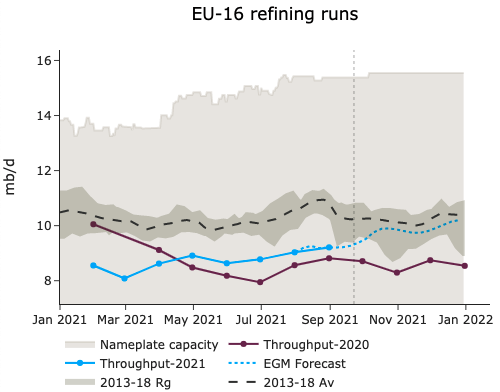

Euroilstocks released EU-16 refining data for August. Runs grew by 150 kb/d m/m, in line with our expectations, at 9.3 mb/d, supported by improved margins. Diesel and jet output especially grew by 199 kb/d, supporting the demand growth in the Atlantic basin, as gasoil cracks are now consolidating above 10 $/b for most of the upward-sloping forward curve.