Prices extended losses

Prices were down again yesterday in most European gas markets as new forecasts confirmed a warmer weather outlook for the rest of this week and…

A new milestone has been reached with the decision of the US and the UK to attack Russia’s revenues from hydrocarbon exports. Of course, they can do so because their imports from Russia are still relatively limited (8% of the total for the US, crude and products), which is not the case for EU countries. But the trend is clearly established. The prospect of Russian oil gradually disappearing from the market has pushed crude prices a little higher: Brent 1st-nearby is trading above $130/b this morning.

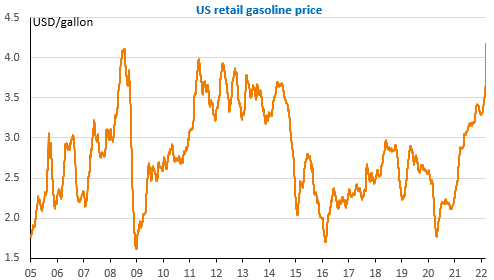

On the domestic front, the US President is taking a risk as gasoline prices have returned to 2008 highs of over $4/gallon just months before the mid-term elections.

The Biden administration is urging shale oil producers to increase production and force the hand of their bankers and shareholders who would restrict financing. The latter denounce a policy that has systematically blocked new drilling on environmental grounds. The US Department of Energy has revised its production forecasts to an average of 12mb/d this year (from 11.6 mb/d at the moment) and 13mb/d in 2023, but it is no longer clear whether this is a forecast or wishful thinking.

According to API estimates, US crude oil stocks rose by 2.8mb last week, but distillate and gasoline stocks continued to fall by 5.5 and 2mb respectively to extremely low levels.