SPECIAL REPORT: Power Market Essentials

DOWNLOAD OUR SPECIAL REPORT Power Market Essentials Power Market Essentials In recent years, the global power market has become a critical component in the transition…

Crude markets continued to be boosted by winter demand expectations, as the ICE Brent November contract reached 79 $/b. The commitment of traders report showed that money-managers increased their net long position by 20 thousand lots, in line with the rally in Dec21/Dec22 spreads, now valued at 7.4 $/b, while the prompt month time spread is valued at 90 cents. We believe this momentum in crude prices and financial inflows will ease as we get closer to the OPEC+ meeting on the 4th of October. This could limit the upward trend in prices, as physical crude differentials remained low and not particularly bid up by the physical players, not reflecting a tightening market.

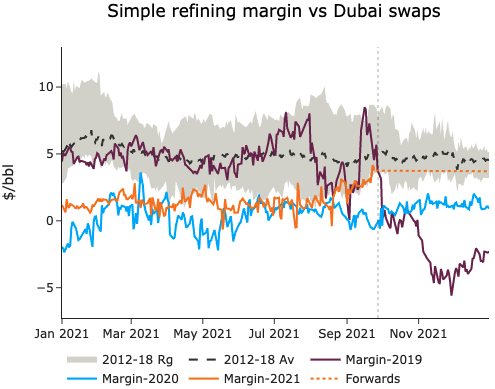

Looking at refined products, middle distillates and fuel oil markets closely followed the crude market rally, which maintained refining margins globally throughout the week. On the jet fuel side, the transatlantic ban travel lifting boosted cracks spreads to reach 9.2 $/b at the prompt against Dated Brent. A 1.2 mb draw in jet stocks at ARA last week also helped to tighten the European jet fuel supply. Gasoil and fuel oil cracks were supported by winter heating demand expectations and high shipping rates boosting shipping demand. In Asia, gasoline prices rallied strongly, with Gasoline prompt time spreads now at 140 cents, which helped margins to be back above the 5-year average profitability levels.