Prices up as geopolitical tensions increase

European gas prices rebounded strongly yesterday, inflated by the rise in the risk premium on the Ukrainian crisis. Indeed, after President Putin recognized eastern Ukraine’s…

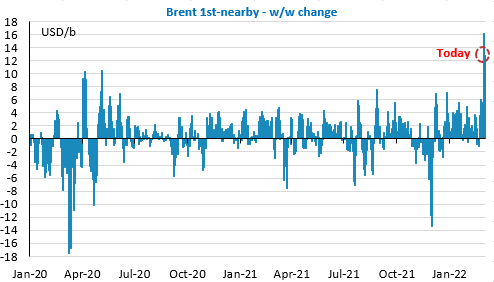

The price of Brent 1st-nearby fell from nearly $120/b to $110/b yesterday. It has risen a little with the events of the night (a missile hit Europe’s largest nuclear power plant in southern Ukraine) which reminds us that the physical risk on the transport of hydrocarbons is always present during armed conflicts. Brent crude oil is now trading at around $111.5/b. However, even after this correction, the price of oil is likely to record a huge weekly rise.

To explain yesterday’s decline, probably already the simple correction of an extremely strong rise in the previous days, and especially the confirmation that an agreement on the Iranian nuclear issue could be announced very quickly, in the wake of the visit of the head of the International Atomic Energy Agency to Tehran. But it should be borne in mind that we are talking about the potential return of 500kb/d of crude oil to the market immediately and potentially 1mb/d in a few months time, while it is potentially the loss of 3 or 4mb/d of Russian oil that needs to be offset. Despite a discount in excess of $20/b and sanctions theoretically calibrated to avoid this situation, it is a fact that Russian oil cannot find a buyer today. This could quickly cause problems of a structural nature as Russia’s storage capacities are much more limited than those of Iran, for example, which could lead to a shutdown of production at certain sites, causing irreversible damage. To make matters worse, production from the main Libyan field (Sharara) is suspended, again due to sabotage and an extremely unstable political situation. Almost 300kb/d are produced at this site.

According to a note from the consultant FGE, the EU is preparing to put some of its 190mb of strategic gasoil reserves on the market to cope with the Russian oil shortage.