Prices down as concerns about payment in rubles abate

European gas prices weakened yesterday. Russian flows increased again, averaging 227 mm cm/day, compared to 218 mm cm/day on Wednesday. Norwegian flows were also up,…

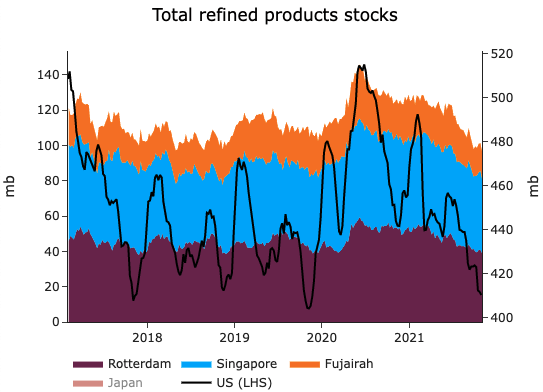

Without material surprises, OPEC+ countries maintained their production policy unchanged yesterday, with 0.4 mb/d monthly production increases considered to be sufficient to respond to a market that will soon be oversupplied in Q1, according to demand estimates and seasonality. Furthermore, OPEC+ members insisted that their decisions could not be challenged by other nations outside OPEC, in clear defiance of the US and other countries prompting the group to increase production. Prices continued to weaken in this backdrop, getting closer to 80 $/b for the front-month ICE Brent contract, as buyers feared a surprise US SPR release that would temporarily oversupply the Atlantic basin market and struggle to clear, given the lack of physical demand for WAF/Urals barrels. As the Saudi Energy ministry noted, crude oil is not responsible for the global energy crisis, given its availability. On the oil side, refined product markets appear to be much tighter than crude markets. Diesel stocks outside the US continued to draw globally at a fast pace last week, with ARA stocks reduced by 0.6 mb, Singapore stocks by 1.2 mb and Japanese stocks by 0.3 mb. Diesel cracks in Europe recovered from their weekly slump after the release of ARA stocks, as low Rhine exports did not even tilt the balance materially leaving the hub undersupplied. Gasoline and naphtha stocks in the two pricing hubs ARA and Singapore are also starting to be quite low, which could further support refining margins in Asia.