Crude prices spike on reports the EU plans to ban Russian oil

Crude oil prices jumped late in the afternoon on Thursday, pushed by reports from the New York Times that the EU is drafting a ban…

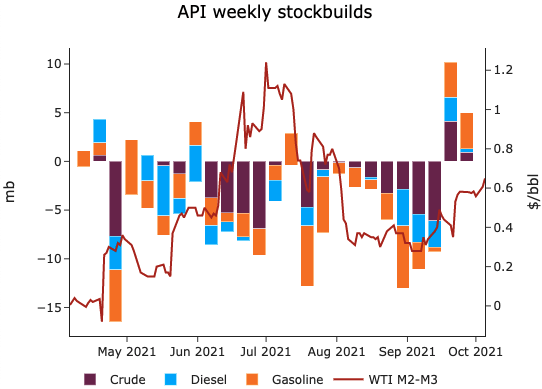

Crude prices rallied yesterday, with front-month ICE Brent futures reaching 83 $/b, as natural gas prices soared in Europe and Asia, putting pressure on diesel and fuel oil winter markets. Yet, US and Japanese inventories increased across the board, with notable builds in US gasoline inventories, according to the API. Japanese crude oil and winter heating fuels were also aligned with seasonal norms, indicating that there is limited upward pressure in the physical market. Front-month time spreads were also rather weak compared to the outright price rally. The 6-month ICE Brent time spread for instance remained range-bound at 4.32 $/b, indicating that the rally in outright prices was only driven by winter demand expectations.

Another sign that indicates that the physical crude market is not as tight as the futures’ market implies is that Saudi Aramco’s official selling prices were slashed yesterday. All grades and all destinations experienced a discount between 1$/b and 0.5 $/b, indicating that Saudi Aramco is concerned about its ability of its customers to fully nominate their long-term contracts.

European gasoil cracks start to be increasingly correlated with natural gas markets, as refiners’ hydrocracker units are exposed to natural gas prices as their primary fuel. The front-month diesel spread has now climbed to 13.2 $/b when the real actual profitability from running diesel production units would be closer to 8 $/b if we account for the cost of producing hydrogen through a steam methane reformer.