Liquidation

Falling inflation expectations, combined with collapsing equities globally, likely triggered a sell-off in crude and refined products futures. ICE Brent prompt contracts for September delivery went…

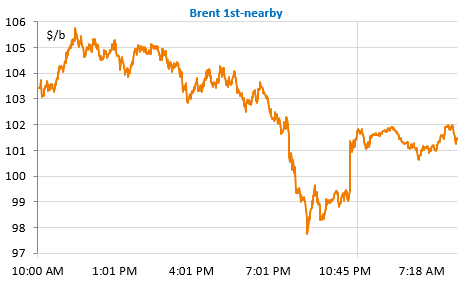

The price of a barrel of Brent crude oil rose yesterday to almost $106, before falling back below $98 and then finally rising back to around $102. Yesterday’s rise is quite understandable. It accompanied Russia’s armed offensive in Ukraine with strong uncertainties about the consequences of sanctions on Russia’s energy exports. It was precisely when Joe Biden detailed these sanctions, which we report on more extensively in the Daily Eco, that the markets realised that the West was not about to jeopardise its own energy supply, even though the Russian economy’s dependence on this sector is clearly its weak point. In addition, the US President confirmed that he was working to bring more strategic oil reserves to market in consultation with other countries.

Then China said it would not join such an initiative. There is also evidence that Russian crude oil, although heavily discounted, is not finding buyers, which certainly reflects a hesitancy on the part of buyers and banks to be sure that these transactions will not fall under the sanctions that have yet to be officially announced by the EU. The fear of a significant drop in supply, even temporarily, is resurfacing and pushing prices up again. The intensification of the fighting in Kiev should keep the market nervous today.

The increase in US crude oil inventories last week (+4.5mb) did not have any impact on the market, especially as inventories fell further at Cushing to a record low. More details here.