Fundamentals likely dwarfed by bond markets inflows

Oil

Crude prices remained range-bound, at 74.5 $/b for the September ICE Brent contract, bond yields continued to slide lower, as the 10y Treasury bond touched 1.24% yesterday. However, this continued outflow from the commodity complex was balanced by strong fundamental data from the US. According to the EIA (detailed content here: Weekly EIA Report – Week to July 2nd), crude inventories dipped by 7 mb, while the US implied gasoline demand hit a historic high of 10 mb/d. US production surprised to the upside, with a 0.2 mb/d weekly increase, at 11.3 mb/d.

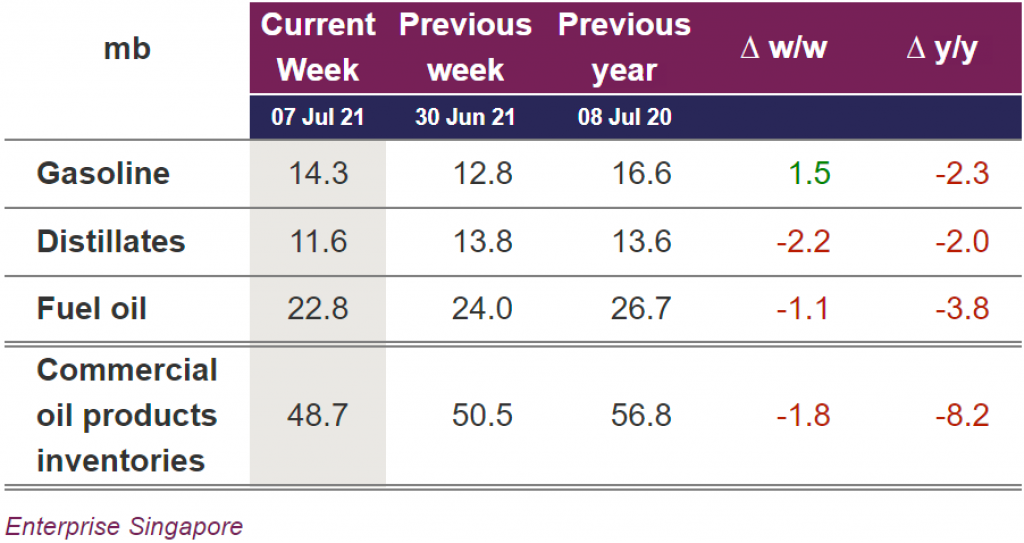

Looking at inventory data in Asia, total product stocks in Singapore declined by 1.8 mb, with gasoline stocks jumping by 1.5 mb, as mobility remained subdued in Asia. Distillates and fuel oil stocks declined respectively by 2.2 mb and 1.1 mb. Strong pulls on fuel oil stocks in Asia and the Middle East (via Fujairah) reflect a strong burning season.

What is happening in the markets is quite unusual: equity markets surged upwards in Europe yesterday before a sharp fall in US indices and relative stability…

European gas prices maintained their bullish momentum yesterday. Norwegian supply rebounded to 341 mm cm/day on average (compared to 331 mm cm/day on Wednesday) after…

Join EnergyScan

Get more analysis and data with our Premium subscription

Crude prices remained range-bound, at 74.5 $/b for the September ICE Brent contract, bond yields continued to slide lower, as the 10y Treasury bond touched 1.24% yesterday. However, this continued outflow from the commodity complex was balanced by strong fundamental data from the US. According to the EIA (detailed content here: Weekly EIA Report – Week to July 2nd), crude inventories dipped by 7 mb, while the US implied gasoline demand hit a historic high of 10 mb/d. US production surprised to the upside, with a 0.2 mb/d weekly increase, at 11.3 mb/d.

Looking at inventory data in Asia, total product stocks in Singapore declined by 1.8 mb, with gasoline stocks jumping by 1.5 mb, as mobility remained subdued in Asia. Distillates and fuel oil stocks declined respectively by 2.2 mb and 1.1 mb. Strong pulls on fuel oil stocks in Asia and the Middle East (via Fujairah) reflect a strong burning season.