Prices up on the spot and the curve

European spot gas prices rebounded yesterday. Despite the drop in residential demand due to the sharp rise in temperatures, weaker pipeline supply left gas balances…

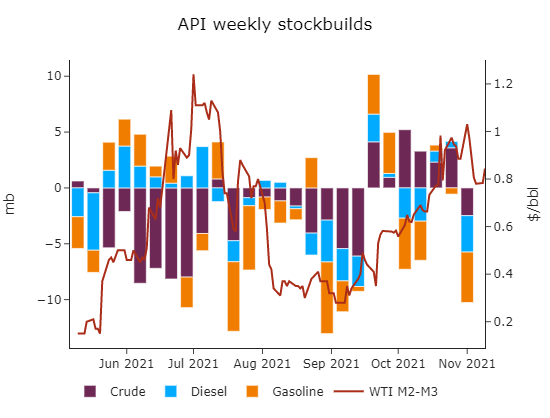

Yesterday’s Short Term Energy Outlook published by the EIA showed a relatively balanced global oil market, with stock builds in H1 22, which was a key report for the US administration to decide whether an SPR release was needed. While the STEO was relatively underwhelming, the API survey showed another set of stock draws across crude, gasoline and diesel products. Such pronounced draws were not experienced since August, with a combined 9 mb stock draw. Crude futures continued to trend higher, with ICE Brent front-month contract rallying to 85.4 $/b amid uncertainty over Biden’s decisions. Time spreads were particularly volatile, reaching 123 cents for F/G Brent spreads while WTI Z/F spreads were trading at 150 cents. We expect significant volatility today as the EIA weekly report will be impactful for Biden’s policy response.