European gas prices mixed, Japan power prices sharply down

European gas prices were mixed yesterday as the rally on Asian markets came to an end but with prices stabilizing at high levels. Indeed, JKM…

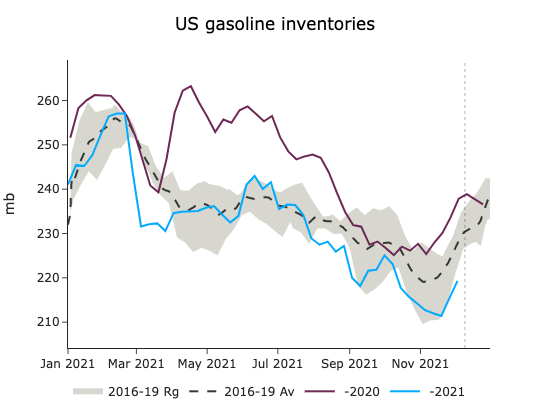

ICE Brent front-month contract trades now above 76 $/b, combined with an unusual worsening backwardation, below 30 cents at the prompt. The recovery in equity markets and declining volatility is boosting outright prices. Yesterday, the EIA showed a higher than average seasonal build in US refined products stocks, with implied diesel and jet demand experiencing sharp declines. If the jet demand level remains at 1.2 mb/d, it could be a first hint at the Omicron demand hit. US crude exports declined to 2.2 mb/d.

These exports, originating from the Gulf coast will soon support a new product launched by ICE, the WTI Midland American Gulf Coast futures, which will be delivered at the Magellan export terminal in Houston. This light sweet benchmark, with potentially 3 mb/d of physically-backed volumes, will challenge Brent’s dominance over the Atlantic waterborne market. The Dated Brent’s methodology and structure continue to be a hot topic for reporting agencies, as dwindling light sweet North Sea supplies are forcing them to consider additional physical streams such as CIF WTI or Norway’s Johan Sverdrup grades to be potentially added to the benchmark. In the meantime, the lack of physically settled volume on the North Sea benchmark could continue to show market squeeze and odd pricing dynamics.