The emissions and power prices tracked the surging fuels markets

The European power spot prices edged up yesterday, supported by the rising fuels and carbon prices, the lingering wind shortage and the solar production expected…

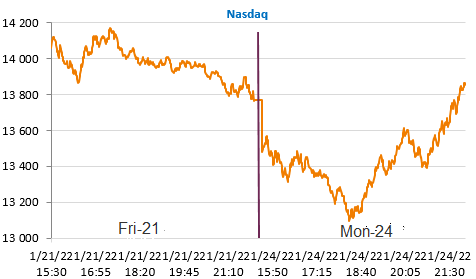

Spectacular reversal of the US equity markets yesterday, which lost more than 4% (for the Nasdaq) in the session and ended the day up. In the meantime, the European markets suffered heavy losses (-4.1% for the Eurostoxx 50).

The causes of this nervousness are known: the approach of the Fed meeting (today and tomorrow) in a particularly tense geopolitical context (Russia) while the real economy seems to have passed the worst of the consequences of the Omicron wave. Market volatility is very high: the VIX index approached 40 yesterday, which has not happened since 2020. The US 10-year rate remains close to its recent lows (1.75% this morning and the EUR/USD near 1.13), which does not indicate much market confidence.

The January PMIs confirmed the very good resilience of industrial activity everywhere but the negative impact of the Omicron wave on services, particularly in the US where the PMI fell to an 18 month low but remained above 50 (50.9).

Today we are awaiting the IFO survey in Germany, CBI in the UK and most importantly, house prices and household confidence in the US. The market should remain very nervous with Russia and the Fed. We will publish a note on what to expect from US monetary policy later today.