EUAs fell further on dropping fuels and supply concerns

The European power spot prices continued to rise yesterday amid forecast of warming temperatures strengthening the demand for cooling and weak renewable production. Prices climbed…

Russian forces appear to be on the verge of taking control of the Ukrainian capital and overthrowing the existing government, in order to install a government that is likely to be totally subservient to Moscow. Uncertainty about Vladimir Putin’s intentions, particularly with regard to other countries in the region, and about the economic consequences of the invasion of Ukraine sent European equity markets plunging yesterday (down nearly 4% on average) while pushing energy prices to new highs. The US dollar also rose sharply, with the exchange rate against the euro touching 1.1106.

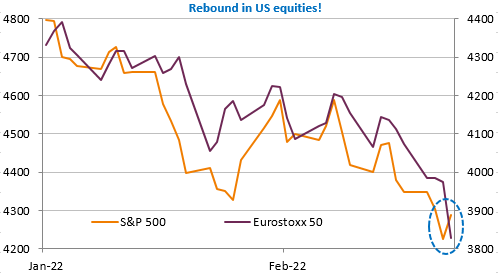

But the trend was completely reversed when Joe Biden unveiled the content of the sanctions taken against Russia: they concern the country’s main banks, several large public or private companies and personalities with great wealth and/or close to Vladimir Putin. The details of these measures can be found here. These measures essentially restrict the ability of these companies or financial institutions to raise funds abroad and conduct foreign currency transactions. There is also a set of measures aimed at limiting Russia’s access to high-tech products as much as possible, which is probably the most effective part of these sanctions. Indeed, at the request of several European countries in particular, Russia retains access to the Swift messaging system used for all international transactions and exemptions are granted for energy and food transactions, among others. Sanctions taken by the EU should be announced officially today but will keep the same principles. In other words, Western governments are not imposing the toughest measures because they are not prepared to bear the consequences (rising inflation or even shortages of essential goods). US equity markets rebounded, with the Nasdaq even rising 3.35%. Long-term interest rates followed suit and the EUR/USD exchange rate rose back above 1.12.

It is remarkable that in such a geopolitical context, central bank rate hike expectations were so little affected. Economic data released this morning can only keep inflation concerns at the forefront with inflation in France accelerating again to 4.1% in February. US private consumption price data should reinforce the trend and the 10 year yield could move back above 2% even as the Russian victory in Ukraine takes shape.