Japanese refiners reduce throughputs

ICE Brent futures contracts remained broadly stable, at 63 $/b, after regaining from Monday’s price slump. The talks to revive the Iranian nuclear deal were…

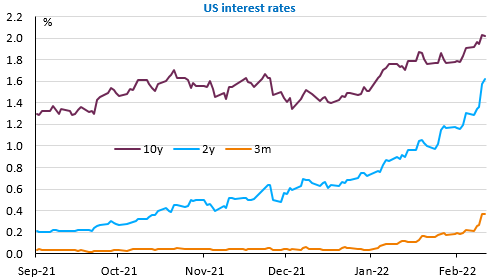

As has been the case for some time, US inflation figures exceeded expectations in January: 7.5% with inflation excluding energy and food at 6% yoy. We haven’t seen such a slippage for 40 years. James Bullard, President of the St Louis Fed, said that the Fed should raise its key rate by 100bp over the next three meetings, reinforcing the hypothesis of a 50bp increase in March. But that’s not all, he suggested that hikes between meetings could occur and finally estimated that the Fed’s balance sheet could be reduced at a rapid pace, possibly involving sales of assets that have not yet matured.

Interest rates accelerated sharply: the 2-year gained nearly 30bp during the session! The 10-year is now over 2%. The USD is strengthening, but not that much (1.1375 against the euro) probably because investors think that the ECB will also strengthen its speech but also because the strong flattening of the yield curve in the United States suggests that a clear economic slowdown is on the horizon.

UK GDP figures released this morning show solid growth (+1% qoq in Q4 2021) and a fairly limited Omicron impact (GDP fell by 0.2% in December). To be followed today, mainly the University of Michigan’s survey of US households (and thus the consequences of inflation).