Omicron storms the markets

A wave of panic swept through the financial markets on Friday in a context of low liquidity. The announcement of the emergence of a new variant,…

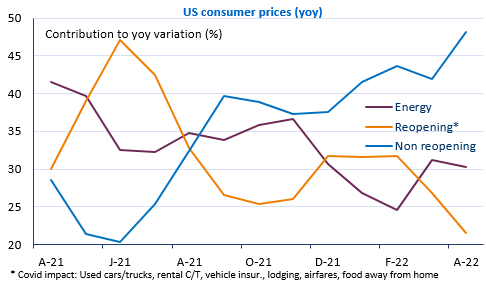

The US inflation rate did fall in April, but only from 8.5% to 8.3%. The core inflation rate fell from 6.5% to 6.2%. In detail, the sharp acceleration in many service prices, aerospace prices and rents shows that the Fed will not be able to rely on this decline in inflation to slow down its monetary policy tightening, at least not in the short term. The cumulative effects of the energy price increases and the end of the pandemic only explain 50% of inflation over one year, which leaves around 4% of inflation explained by structural causes (wage pressures, industrial bottlenecks). This is twice the central bank’s target. The yield curve is flattening out again. This is known as “bull flattening”, i.e. this reduction in the gap between rates on long maturities (such as the 10-year) and those on short maturities (2 years) is achieved by the fall in long rates: the 10-year has fallen back to 2.86%. In other words, the market thinks that the Fed will indeed have to tighten its policy significantly to calm inflation and that this will eventually lead to a sharp economic slowdown. Equity markets are falling.

The ECB is also preparing to raise its key rates and probably as early as July as its President suggested yesterday. But the market was already anticipating this and it did not support the euro against the dollar: the EUR/USD exchange rate is testing the 1.05 support again this morning.

The British pound is also down despite a clear outperformance of the UK economy in Q1, with GDP up 0.8% qoq. But the market was expecting more and more importantly, GDP fell in March due to the impact of inflation on consumption. The EUR/GBP exchange rate rose above 0.86.

More US price figures today with the PPI and weekly jobless claims.