Strong price rebound

European gas prices rebounded strongly yesterday, supported by cold weather, ongoing concerns on Russian supply and technical buying. The rise in Asia JKM prices (+3.01% on the…

Sometimes markets are fascinating (or despairing?). It was enough for the Fed Chairman to be reassuring about 1) the Fed’s desire to curb inflation and 2) its ability to do so without breaking growth (i.e. by raising rates to a minimum) for the equity market to rebound and for long rates to ease somewhat (the 10-year is back at 1.74%). Knowing that the Fed was constantly denying the inflationary risk until September after having made a major strategic change during the summer of 2020, which led it to openly display the objective of creating the conditions for a higher inflation rate, this seems surprising and imprudent, to say the least. In fact, the Fed has made an about-face over the past two months that looks more like a hasty adjustment in the face of facts that stubbornly defy its reassuring rhetoric than a well-considered choice.

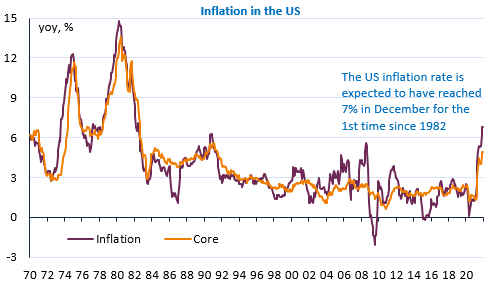

US inflation is certainly expected to fall in 2022, but the question is how much and whether core inflation will also fall significantly. For the time being, a new record high is expected in December, with the consensus being 7% for headline inflation (highest since 1982) and 5.4% for core inflation (highest since 1991).

The USD fell slightly against the euro to 1.1360.