Sharp price rise

European spot gas prices increased sharply yesterday on tighter supply while the strong rise in temperatures is expected to stimulate air conditioning demand. The increase…

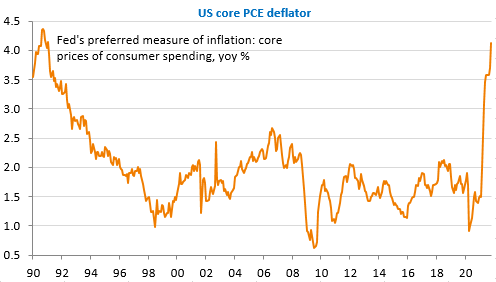

The avalanche of statistics published yesterday in the US before the long Thanksgiving weekend confirmed the reacceleration of activity and growing inflationary pressures: higher than expected household spending and income in October, rebound in investment (durable goods orders), lowest level of unemployment claims since 1969, but a drop in household confidence due to inflation whose preferred Fed’s measure (“core PCE deflator”) reached its highest level since 1990 (4.1%).

The Fed Minutes showed that the possibility of accelerating the exit from QE had been discussed. The probability of such a measure being announced as early as December is increasing and the markets are now anticipating a first increase in the Fed funds rate as early as June 2022. The only significant factor that could change the situation is the accelerated rebound of the Covid epidemic after Thanksgiving…

In Germany, the SPD-Green-FDP coalition has agreed on a governing program more quickly than expected: it is a mixture of very ambitious (unrealistic?) objectives in terms of energy policy to combat global warming, strong social measures (25% increase in the minimum wage)… and budgetary rigour, including at European level. How will all this work in practice? The question remains. But from the ECB’s point of view, there are ingredients for more inflation (increase in wages, social minima, price of CO2) that will strengthen the position of the “hawks”.

The EUR/USD exchange rate fell below 1.12 yesterday before rebounding. The economic agenda is light but the proceedings of the last ECB meeting will be published and several central bankers will speak today.