Electric spillovers

Futures crude markets continued to rise on early Monday, with WTI crude prompt prices nearing 81 $/b at the prompt while ICE Brent futures climbed…

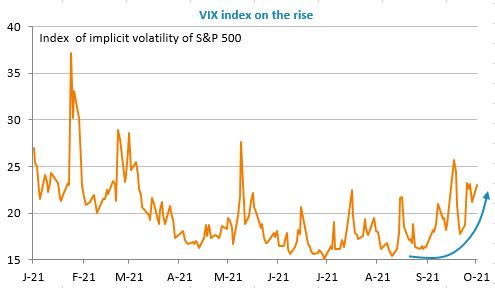

Equity markets continue to decline, particularly tech. stocks: the Nasdaq fell by more than 2% yesterday and is down more than 7% from its early September highs. Inflationary fears were boosted yesterday by the surge in oil prices, so that the US 10-year yield rose above 1.50%, before easing again as concerns about growth took over. Caught between inflation and moderating growth, the markets have entered a period of increased volatility.

After a rise to 1.1640 that was difficult to explain yesterday, the EUR/USD exchange rate returned to around 1.16.

French industrial production grew more than expected in August (+1% mom), notably thanks to the automotive sector, whose activity nevertheless remains 20% below its pre-crisis levels. Today, we are still waiting for the PMI and ISM in services, the US trade balance and producer prices in the euro zone.