EUAs failed again to close above 70€/t

The European power spot prices continued to rise yesterday, supported by forecasts of weaker wind and solar generation and colder temperatures strengthening the power demand.…

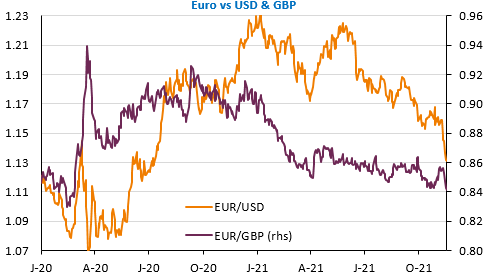

The publication of very good activity data in the US reinforced the rise in bond yields (the US “10 year” has recovered 20bp in 4 sessions) and pushed the dollar to its highest level since July 2020. Retail sales rose by 1.7% in October and industrial production rose by 1.6%. The NAHB housing market index rebounded by 3 points in November, returning to its levels of the beginning of the year. According to the Atlanta Fed’s estimates, GDP growth could rebound to 8.7% in Q4. For completeness, we should add that the yoy growth rate in import prices reached 10.7% in October, which will continue to push up the inflation rate.

Conversely, the euro continues to fall: markets seem to agree with the ECB President’s speech that inflation will fall rapidly in 2022. Moreover, the epidemic recovery is clouding short-term growth forecasts. The euro’s effective exchange rate is at its lowest since May 2020 and the EUR/USD exchange rate fell below 1.13 overnight. The EUR/GBP exchange rate also broke through 0.84 for the first time since February 2020. The acceleration of inflation to 4.2% yoy in October in the UK clearly increases the probability of a BoE rate hike in December.

Today, the final Eurozone inflation figures for October and the US construction figures for October. The main reports expected this week have already been released.