Central banks move forward, despite omicron

After the Fed, which accelerated the exit from QE, the Bank of England took the markets by surprise for a second consecutive time by raising its key…

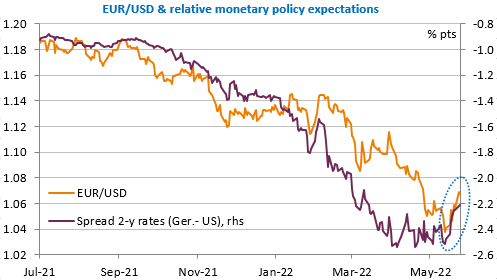

It seems that as soon as Mrs Lagarde speaks, the euro rises. This was the case yesterday and it is happening again this morning after an interview with Bloomberg. The EUR/USD exchange rate rose from 1.0550 to over 1.07. What did she say? That the ECB would probably raise its key rate by 25bp in July and that the rate would no longer be negative at the end of September (which would imply a further 25bp rise in September). This is exactly what the market was expecting and it seems that some ECB members even feel “trapped” after these statements as they would be in favour of a faster rate hike. But it is true that the ECB President had not yet been so explicit. We must add the fact that two members of the Fed also felt that, after having raised the key rate to 2% this summer, the Fed should adjust its policy according to inflation (which should fall), and that a pause would be welcome at the end of the summer. As a result, rate spreads are narrowing, especially on the 2-year maturity, which is now supporting the euro.

The other factor in the rise is confidence, which returned to the markets yesterday, particularly following the announcement of stimulus measures by the Chinese authorities. But this effect was short-lived, judging by the reversal of the trend on the Asian markets. On the contrary, it is the multiple downward revisions of growth forecasts to 3% this year, or even less (against an official target that is still +5.5%) that have taken over.

Today, the preliminary PMI indices will be released in the wake of a German IFO survey that was slightly better than expected yesterday and a fairly stable INSEE survey in France. In general, the business climate seems to be more resilient than expected to the consequences of the war in Ukraine, as we pointed out in the latest Macro & Oil Weekly Report.