TTF CAL 2023 prices above the €100/MWh mark

Bulls kept control of European gas prices on Wednesday with concerns over a slowdown in storage injections in June (see below chart) due to the drop in…

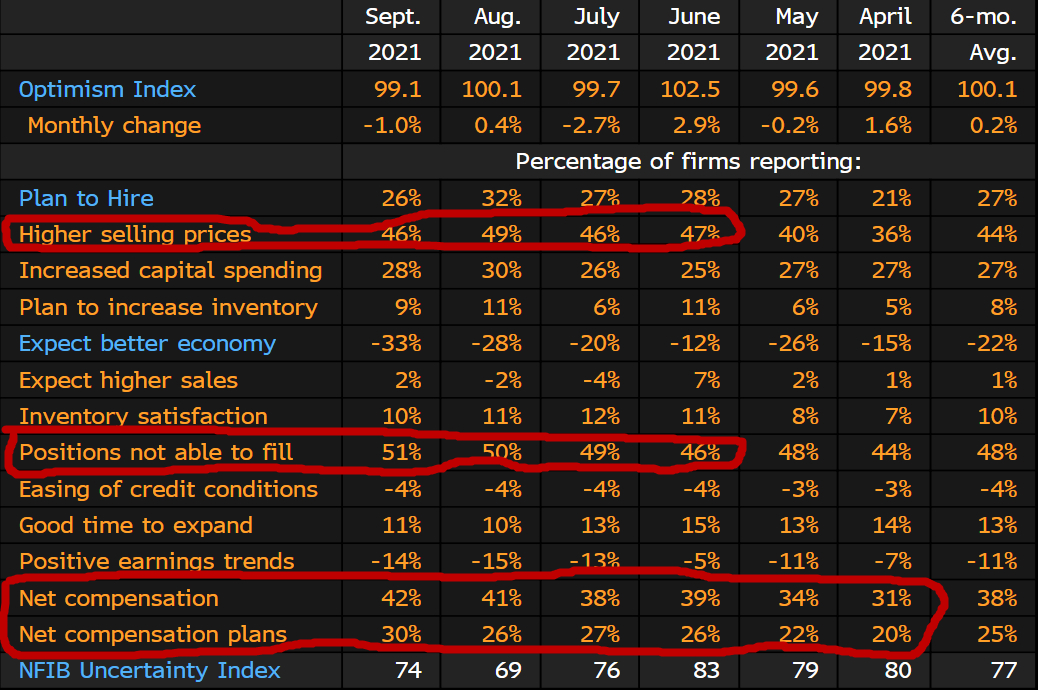

The US 10-year yield eased slightly below 1.6% despite surveys showing increasing inflationary pressures. We mentioned the Bank of France survey yesterday, the main findings of which can be found here. But the NFIB survey of small businesses in the US also found that hiring difficulties are at an all time high and companies are planning to raise wages and selling prices in the coming months.

>

>The UK employment figures say the same thing and the New York Fed survey confirms that consumers expect inflation to be sustained. According to the Atlanta Fed Governor, it is no longer appropriate to use the term “transitory” to describe the current inflationary surge. Perhaps the bond market is afraid of being caught off guard by today’s US inflation figures for September: the consensus forecast is for headline and core inflation to remain stable at 5.3% and 4% yoy.

Apart from US inflation, the news is rich: we already had last night China’s foreign trade in September showing a re-acceleration of exports to +28.1% yo- and a drop in imports to +17.6%. Given the base effects and volatility, these statistics are difficult to interpret. In the UK, GDP recovered in August (+0.4%), but less than expected and especially after a negative July (-0.1% vs +0.1% previously estimated). This makes an early tightening of monetary policy all the more risky. The GBP does not seem to be reacting but could take a hit today. Eurozone industrial production is expected to fall in August, mainly due to supply problems in the German car industry. Finally, the day will end with the publication of the Minutes of the last Fed meeting. Volatility could be quite high in the markets today. The USD has resumed its slightly upward trend, but is not far from 1.1550 against the euro.