Gas & Power Report: Energy prices remain under bearish pressure in Europe

Gas & Power Podcast #45 In this week’s Gas & Power podcast, Julien Hoarau discusses about the reduction of the contango on the EU as…

Financial markets continue to move in tandem with news from the Russian-Ukrainian border. At the end of last week, there was widespread pessimism ahead of a Russian attack that the US administration said was “imminent”. The French and German governments called on their citizens to leave Ukraine. The trend reversed overnight after the Russian and US Presidents agreed in principle to a Summit proposed by the French President (on condition that Russia did not launch a military offensive in the meantime). Futures rebounded on the equity markets and the US dollar fell sharply (from 1.131 before the news to 1.1375 now against the euro). Bond yields are little changed.

What happens in Eastern Europe should remain the main market mover today, especially as US markets are closed for Presidents Day. Japan’s services PMI plunged in February due to the Omicron wave, but activity should soon recover. The 1st estimates of the Eurozone and UK PMIs will be released as well today, but Improvement is expected in services. The UK Prime Minister is expected to announce today the end of the anti-Covid measures.

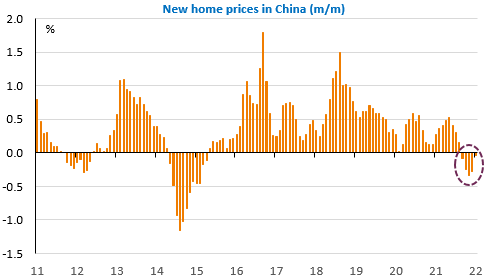

China’s property prices fell for the fifth month in a row and the new default of a property developer considered among the strongest is a major concern.