2022 Energy Markets Outlook

The EnergyScan team held its quarterly webinar covering key trends and events on energy markets. In this webinar, our experts addressed the following topics, with…

ising equities, slightly easing bond yields, falling USD: optimism prevails despite the sharp slowdown in the Chinese economy highlighted yesterday by the Q3 national accounts. Concerns about rising inflation pushed the US 10-year yield up to 1.62%, but it then eased back to 1.57%. The EUR/USD exchange rate returned to its highest level since late September, around 1.1650.

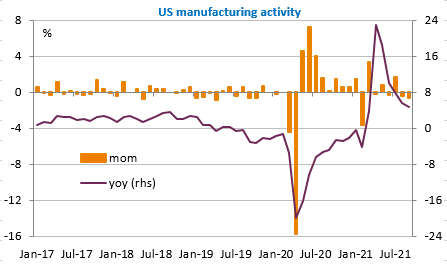

US industrial production contracted by 1.3% m/m in September, mainly due to a sharp decline in the automotive sector (-7.2%), as in most countries.

According to the Chinese Ministry of Industry, the shortage of semiconductors should ease, but it should also limit domestic car production. The effects of Covid, on the other hand, seem to be dissipating well in the US, as evidenced by the sharp rise in the NAHB housing market index, while loan rates are rising.

The economic calendar is light today. Construction data is expected to fall in the US. But the markets should continue to focus on corporate earnings and central bankers’ statements, especially in the UK where a rate hike is expected as early as next month.