Global gas prices correct downwards

European gas markets experienced another strong upward move on Monday as transport capacity auctions for the next gas year closed at noon with no capacity…

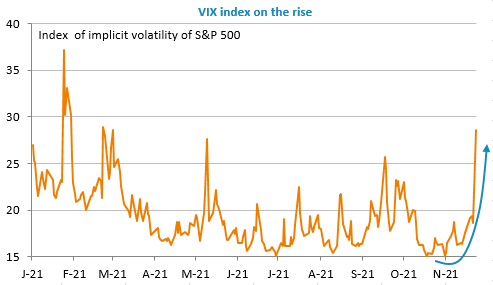

A wave of panic swept through the financial markets on Friday in a context of low liquidity. The announcement of the emergence of a new variant, henceforth referred to as “Omicron”, with multiple mutations, apparently highly contagious and potentially resistant to existing vaccines, led to a sharp fall in the equity markets (-4.7% for the Eurostoxx 50, -2.3% for the S&P 500 with a risk index, the VIX, up by more than 50%), a clear downward revision of the prospects for monetary tightening and a marked fall in bond yields, with the US 10-year falling from 1.63% to 1.47%. This decline was accompanied by a fall in the US dollar, which had previously benefited from its status as a safe haven during episodes of heightened risk aversion: the EUR/USD exchange rate rose back above 1.13. Finally, oil prices have fallen sharply.

The economic impact of this news will already be significant in the current quarter as many governments have taken restrictive measures, particularly with regard to travel, while waiting for more information. The entire holiday season appears to be at risk.

The markets seem to be regaining some composure this morning because, after all, nothing is certain, particularly with regard to Omicron’s resistance to vaccines. A positive announcement on this front would probably be enough to trigger a broad-based rebound, but the next few days are likely to be marked by high volatility as markets oscillate between inflationary risk and fears of a relapse in activity. Germany’s November inflation figures are released today and are likely to be above 5%.